The goal of any investor is to accumulate wealth to fulfill future wants and needs. Many of the conservative investors choose Bank Fixed deposits as they think it is a safe investment option. While there is no doubt that Bank Fixed Deposits come with the highest safety, the biggest disadvantage about them is Tax. In this article we have listed alertnatives to Fixed Deposits, some of the most common debt instruments, along with their features, how they score on various parameters and which type of investors will find them useful. Find out which of these instruments suit you best.

Table of Contents

Why Look Beyond Bank Fixed Deposits

For a conservative investor, protection of principle is of utmost importance. Many of the conservative investors choose Bank Fixed deposits as they think it is a safe investment option. While there is no doubt that Bank Fixed Deposits come with the highest safety, the biggest disadvantage about them is Tax. Interest on Fixed Deposit is fully taxable so if you happen to be in the highest tax bracket you pay upto 30.6% tax on the interest income. If a person is in the highest tax bracket, the post tax yield of a 9% fixed deposit comes down to 6.3%. And if you break it before the tenure of the fixed deposit you may have to pay penalty for premature withdrawal. Focusing only on the interest rate offered could backfire if one doesn’t examine the tax treatment of the returns, or the liquidity and flexibility offered by the product. Before investing, one should understand how the product works, how liquid it is and if there is a penalty for premature withdrawal.

Are there alternatives to Bank Fixed Deposits? Yes there are

- Public Provident Fund (PPF), Tax-Free Bonds, which are tax-free options

- Bank Recurring Deposits Company Deposits, Company Debentures which are taxable as per your income slab.

- Fixed Maturity Plans (FMP), Debt Mutual Funds which are taxed on maturity or withdrawal but you can use indexation benefit

Due to lackluster returns/volatility of the stock market and higher interest rates/tax free options offered by FMPs and tax-free bonds, In FY 2013-14 tax free bonds, Fixed Maturity Plans were lapped up by investors. Some even liquidated assets to invest in these bonds that will give tax-free returns for 15-20 years. After the issues dried up in the primary market, most bond prices went up by 2-3% in the secondary market. But Investors who stocked up on these long-term bonds and FMPs can get into a tricky situation if they have to exit their investments prematurely in an emergency. Because FMPs and tax-free bonds, though listed on the stock exchange, are extremely illiquid and rarely traded on exchanges. One is often forced to sell at a huge discount. Our article in Think about Liquidity,Safety,Returns,Risk,Tax explains in detail about what should one look for in investment product.

Investors can reduce the tax on their debt investments in other ways as well. For example, investors can opt for the indexation benefit to maximise their returns. Indexation takes into account the inflation during the holding period and accordingly reduces the tax.

Investors can also use capital losses—both short-term and long-term—they have incurred to bring down their tax liability. You can carry forward them for next eight years and use them to reduce the tax liability arising from capital gains in the coming years. Let’s look at Bank Fixed Deposit

Bank Fixed Deposits: Taxed every Year

Fixed Deposit(FD) is an investment product which allows you to invest a lump of money for a fixed time period and at a fixed rate of interest. Our article Overview of Fixed Deposits explains about Fixed Deposits. Articles related to FD ex FAQon Tax and Fixed Deposits, Premature withdrawal or Breaking of Fixed Deposit are organised at Learn about Investing

RETURNS:7-8% per year.

SAFETY: High. because banks tightly regulated; deposit insurance of Rs l lakh per

LIQUIDITY: Very high. You might have to pay penalty charges.

FLEXIBILITY: Very high. You can invest as little as {500, with no upper limit. Online transactions add to the convenience.

TAXATION: Income is fully taxable, so post-tax returns not attractive for investors in higher tax bracket.

BEST FOR: Risk-averse investors with income up to Rs 5 lakh a year. High liquidity and flexibility make fixed deposits an ideal place for your contingency fund.

SMART TIP Invest in fixed deposits of banks that do not charge/charge less penalty for premature withdrawals.

Alternatives to Fixed Deposits: PPF, a Tax Free Option

Public Provident Fund (PPF) is one of the safest forms of investment. Public Provident Fund (PPF) is a long-term ( 15 years), government backed small savings scheme Our article Understanding Public Provident Fund, PPF, On Maturity of PPF account, PPF Account for Minor and Self etc covers different aspects of PPF which are organised at our Investing webpage. Features of PPF are as follows:

RETURNS: 8.7% for 2014-15. Linked to bond yield. 50 it can vary in future.

SAFETY: Very safe because it’s backed by the government.

LIQUIDITY: Moderate. Term is 15 years but you can make partial withdrawals after 6 years or take a loan after 3 years

FLEXIBILITY: Moderate. Investment ceiling 0f 1 lakh per year for an individual. Minimum investment per year is Rs 500.

TAXATION: Eligible for deduction under Section 80C. Interest is completely tax-free.

BEST FOR: Conservative investors looking for tax deduction. assured returns and tax-free corpus on maturity

SMART TIP : Invest before the 5th of the month so that the investment gets interest for that month as well.

Alternatives to Fixed Deposits: Tax-free bonds, a Tax Free Option

Tax free bonds are those bonds issued for long term, for investment horizon of 10 to 20 years. Tax free bonds do not provide any benefit of tax savings but only interest earned on these bonds is tax exempt. The interest on these bonds is paid annually on a fixed date and one gets the invested amount at maturity. Our article Understanding Tax Free Bonds explains tax free bonds in detail. Tax Free Bonds of FY 2011-12, FY 2012-13, Tax free Bonds of FY 2013-14 deals with tax free bonds in detail. Features of Tax Free Bonds are given below.

RETURNS: 8.25-8.5% per annum. Potential to earn capital gains in secondary market

SAFETY: High because the issuers are Public Sector Units (PSU) companies.

LIQUIDITY: Moderate Bonds are for 10-20 years, but they are listed on exchanges, so one can sell in the secondary market.

FLEXIBILITY: High because retail investors can put as little as Rs 1,000 (price of one bond) and up to Rs 10 lakh. Investment of over Rs 10 lakh fetches a marginally lower interest.

TAXATION: While interest is tax-free, any capital gain from selling bonds in secondary market will be taxed at 10%. No indexation benefit available.

BEST FOR: High-income investors who want tax-free income and are willing to lock in for the long term. Who can also invest the interest amount received yearly.

SMART TIP : Invest in bonds with a large issue size (minimum 2500 crore) as they are more liquid than bonds of smaller issues.

Alternatives to Fixed Deposits: Bank recurring deposits

Recurring Deposits (RD) are a special kind of Term Deposits offered by banks in India in which people deposit a fixed amount every month into their Recurring Deposit account and earn interest. It is similar to making Fixed Deposits (FDs) of a certain amount in monthly installments, for example Rs 1000 every month. This deposit matures on a specific date in the future along with all the deposits made every month Our article Overview of Recurring Deposits covers RDs in detail.

RETURNS: 8.5-9.5% per year.

SAFETY: High, because banks are tightly regulated and deposit insurance of up to Rs 1 lakh per bank.

LIQUIDITY: High. Most banks don’t slap a penalty for breaking an RD. You only get a reduced interest rate.

FLEXIBILITY: High. You can invest small amounts, and for up to 10 years.

TAXATION: Though there is no TDS, the interest is fully taxable at normal rates. Post-tax yield for high income bracket is not very attractive.

BEST FOR: Investors wanting to accumulate a predetermined amount by a specific date.

SMART TIP Instead of one large deposit. have multiple deposits, so that even if you close one early, others continue.

Alternatives to Fixed Deposits: Company deposits

Company fixed deposits are offered by corporates that are linked to their businesses and are tied-in to the profits of the company. Our article Company Fixed Deposits : 5 Ways to Benefit from Corporate FDs covers how can one benefit from Company Deposits.

RETURNS: 9-12%

SAFETY: Moderate to low. depending on the Credit rating assigned to the deposit.

LIQUIDITY: Low because premature withdrawal could take weeks.

FLEXIBILITY: Moderate to low. Available in fixed denominations. You can invest up to Rs 1,000 with no upper limit. Few companies offer online investing facilities.

TAXATION: Like FDs, the interest is fully taxable, so post-tax yield is low in 30% tax slab

BEST FOR: Retirees wanting higher interest who can lock in the money for full term.

SMART TIP Don‘t invest in deposits rated below AA. Even then. don’t invest for very long terms of more than 5 years.

Alternatives to Fixed Deposits: Company debentures

Debentures is a document that either creates a debt or acknowledges it, and it is a debt usually without physical assets or collateral. Our article What are Non Convertible Debentures or NCD? explains it in detail.

RETURNS: 9-12%

SAFETY: Moderate to low. depending on the credit rating assigned to the issue.

LIQUIDITY: Moderate. Since they are Listed on exchanges, liquidity is better compared to company fixed deposits. You may have to sell at a discount if liquidity is low.

FLEXIBILITY: Moderate to Low. Available in fixed denominations. You can invest up to {1,000 with no upper limit. Few companies offer online investing facilities.

TAXATION: Interest is fully taxable at normal rates so investors in high income slabs won‘t find them attractive. Capital gains taxed at 10%. There is no indexation benefit.

BEST FOR: Savvy investors who can time the markets and earn capital gains.

SMART TIP Go with high rated papers and issues with large size around Rs 500 crore) which are more liquid.

Alternatives to Fixed Deposits: Debt mutual Funds Tax but with Indexation

A debt mutual fund is an active mutual fund, which invests money in government securities, bonds, money market instruments and corporate deposits. They include a small percentage of equity investment of around 10% in their portfolio to give investors capital appreciation. Hence, debt funds are associated with little or limited investor risk. Our article How to Choose Mutual Fund explains how to choose mutual funds. Features of Debt Mutual funds are :

RETURNS: 8-10% per annum.

SAFETY: Moderate. Diversification reduces the default risk but interest rate risk remains.

LIQUIDITY: High. The redemption reaches your bank account in a few days.

FLEXIBILITY: High. After the initial investment of 25000-10000. you can invest in small denominations of {SOD-1,000 and redeem whenever you like. Online facility also available.

TAXATION: Gains taxed as normal income if holding period is less than a year. If over a year, tax is 10% flat or 20% after indexation.

BEST FOR: Investors in the high income bracket who are looking for liquid but tax-efficient.

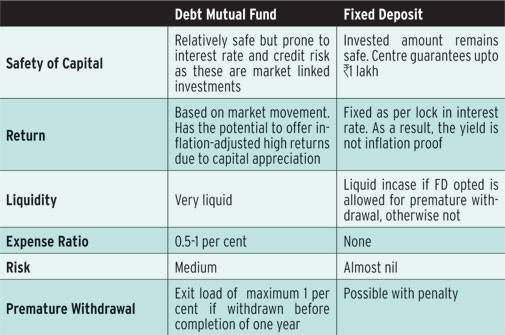

Following image compares FD with Debut Mutual Funds

Alternatives to Fixed Deposits: Closed-ended FMPs tax but with Indexation

Fixed maturity plans are closed-ended income schemes by Mutual Fund houses that invest in fixed income instruments or debt securities with maturity coinciding with the maturity of the scheme. Our article What are Fixed Maturity Plans (FMP) explains it in detail.

RETURNS: 9-95% per annum.

SAFETY: High. Diversification cuts default risk, while holding till maturity cuts interest rate risk.

LIQUIDITY: Low. FMPs are locked till maturity. Though they can be traded on exchanges, the volumes are very low.

FLEXIBILITY: Moderate. Minimum investment is Rs 5,000. FMPs available from 1 month to 3 years. Can be purchased online as well.

TAXATION: Like debt funds, they are more tax-efficient than FDs and recurring deposits.

BEST FOR: Investors looking for tax-efficient returns and willing to hold till maturity.

SMART TIP : Buy FMPs that straddle more than two financial years so that you maximise the indexation benefit.

Indexation

Inflation is an increase in the price of a basket of goods and services. Indexation takes into account the inflation during the holding period and accordingly reduces the tax. It is available on investments for more than a year. The indexation benefit is calculated on the basis of the financial year in which the investment was bought and sold. Smart investors use this by investing at the fag end of the financial year and redeeming at the beginning of another financial year. So, a 13-month FMP bought in March 2014 and maturing in April 2015 will qualify for double indexation benefit. This reduces the tax to almost nil or give you a credit in the form of a capital loss that can be set off against other gains. Our article Cost Inflation Index,Indexation and Long Term Capital Gains explains in detail. Following picture shows how indexation helps.If say one invests a amount of Rs 10 lakh at 9% returns for 1 year. 8% is rise in consumer calculation.

| Fixed Deposit | With 10.3% flat | With Indexation | |

| Amount Invest | 1000000 | 1000000 | 1000000 |

| Income(Interest) | 90000 | 90000 | 90000 |

| Taxability | Fully taxable | Only gains are taxable | Only gains are taxable |

| Taxable Income | 90000 | 7431 | 826 |

| Tax rate | 30.9% | 10.3% flat | 20.6% after indexation |

| Tax payable | 27,810 | 765 | 170 |

Related articles:

- PPF related articles Understanding Public Provident Fund, PPF etc covers different aspects of PPF which are organised at ourInvesting webpage

- FD related articles such as FAQon Tax and Fixed Deposits,Premature withdrawal or Breaking of Fixed Deposit are organised at Learn about Investing

- Inflation Calculator , Capital Gain Calculator and more calculators can be accessed from our Menu of Calculators and Quiz.

- Capital Loss on Sale of House

Choose an investment option which optimises returns, ensures liquidity and minimises tax without compromising on safety. And make sure the investment fits into one’s overall financial plan.Other than FD which is your favourite fixed income option.

11 responses to “Alternatives to Fixed Deposits: PPF,FMP,Debt MF,RD,CD”

Dear Team,

Thanks for the informative article. Have a question: On the example under ‘Indexation’, how is the taxable amount of Rs 7431 (as ‘only the gains are taxable’) arrived at?

Thanks!

Hi

Thanks for this detailed resourceful post on options better than traditional FD which are safe as well as give good returns

Thanks Karan. Sadly people don’t move beyond Fixed Deposits and don’t realise that interest is taxed 🙁

Hi

Thanks for this detailed resourceful post on options better than traditional FD which are safe as well as give good returns

Thanks Karan. Sadly people don’t move beyond Fixed Deposits and don’t realise that interest is taxed 🙁

Yes (MULTI OPTION DEPOSIT SCHEME or Auto Sweep Account)

Yes (MULTI OPTION DEPOSIT SCHEME or Auto Sweep Account)

Good article. Thanks. Though MOD is also a kind of fixed deposit, Can this also be added as a SEPARATE candidate? (Awareness Sake)

Sure Sir.

Anything that raises awareness to readers can be and should be added.

By MOD did you mean MULTI OPTION DEPOSIT SCHEME popularly known as Auto Sweep Account?

Good article. Thanks. Though MOD is also a kind of fixed deposit, Can this also be added as a SEPARATE candidate? (Awareness Sake)

Sure Sir.

Anything that raises awareness to readers can be and should be added.

By MOD did you mean MULTI OPTION DEPOSIT SCHEME popularly known as Auto Sweep Account?