Bemoneyaware book on teaching Money to Children is now available on Amazon and Flipkart priced at Rs 199. This article talks about why we should teach our Children about Money and talks about the book. If you don’t teach your kids how to manage money, somebody else will. Is that a risk you want to take? Teach your kids how to handle money now, and they won’t end up with money regrets later on in life. You can give them the head start you wish you’d had.

Table of Contents

Excerpts from the book

We have also launched a new website bemoneyaware.com for covering money concepts such as Need vs Wants, Credit cards in detail.

We are also having a contest for children and parents to contribute their articles on the new website. So do visit bemoneyaware.com

| Is Money Everything | Needs and Wants | How Do People Earn Money? |

| Credit Cards and Debit Cards | Rich and Poor Countries | Banks in India |

|

The book is available as a paperback on Amazon, Flipkart and Notion press for Rs 199 + Shipping Charge. Discount Coupon: Get it for Rs 150 (+ Shipping charge) if you order from here. Coupon Code: BOOKLAUNCH2018 |

Let’s Learn About Money book

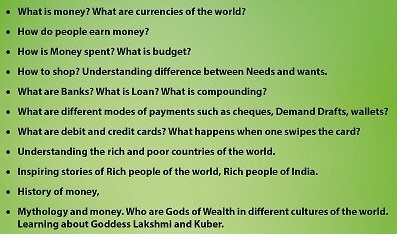

This book covers the following concepts with interesting stories, information.

Book Lets Learn About Money contents

Why should we teach our children about money?

“Just go to the ATM and take out the money,” after I told my son I couldn’t buy a toy he wanted. I realized it was time to explain to my children where the money comes from. After all, it’s up to parents to teach their kids smart financial habits. And I don’t want them to grow up to be like me. I remember how my hands shook when I signed my first cheque. My first salary I just gave it to my parents. How many of us wish we would’ve been taught more about money in childhood?How many of us look at our children and wish we could teach them about money? We spend so much energy to ensure that our kids are successful in life and become independent, but are we equipping them with sound financial habits?

There are two ways of looking at teaching kids about money:

- Many people feel that we should not speak to children about money, as they feel they were not taught about the same by their parents. They learnt it as they were growing up.

- There is another group of people that feels that children should be spoken and taught about money. “Rather than give a hungry man a fish, it is far better to teach him to fish for himself, then he will have food of his own for lifetime”

Your kids will learn about money from someone. Don’t let your children learn half-baked knowledge on money from friends, some celebrity on social media. Money shouldn’t be a taboo subject, and no, your kids don’t need to be sheltered from financial matters. You should view teaching your children to handle money in the same way you view teaching them to bathe and brush their teeth—as a necessary skill for life. If your child graduates from high school and his only skill set consists of playing video games, whining, copping an attitude of entitlement, and eating junk food, you have set him up to fail. Are you children growing up thinking money is free. Do they expect their parents to keep paying their bills into adulthood, or they think the government exists to care for them?

You can either teach your children how to handle money or they will struggle in the world where common sense isn’t common. We feel inept that we have not been taught about money or how money works. People who also have a healthy understanding of wealth—don’t obsess about money or worship money. They are, however, careful about how it is handled, and they make sure their children know how to handle money. And You have the opportunity to be the positive example in their lives and be a voice they can trust. So just have the talk with them about money or go deeper if you’ve only skimmed the surface. When is the best time to talk to your kids about money? Right now. Children are sponges—they are going to absorb whatever is around them, so we need to be intentional about what surrounds them. You should view teaching your children about money in the same way you view teaching them to bathe and brush their teeth—as a necessary skill for life.

Let’s Learn About Money Book

We have written the book on helping children learn about money. Actually, that’s how bemoneyaware started, the discipline of writing an hour every morning before preparing to send children to school.

Chapters:

- What is Money

- History of Money

- Earning Money

- Spending Money & Shopping

- Bank

- Mode of Payments in India

- Plastic Cards

- Money and World

- India

- Mythology & Money

Did you know Money comes from Latin word Monte, which means the place in Rome where money was first made & stored

What is Money?

In everyday speech we use the word “money” in a variety of ways, such as “My father makes a lot of money,” or “Bill Gates has more money than anyone else,” or “Reliance Industries” made twice as much money this year as last.” Lets see what does money in each of the sentences mean.

- “My father makes a lot of money,” – money means income or how much does my father earns.

- “Bill Gates has more money than anyone else” – means how much wealth Bill Gates has.

- “Reliance Industries made twice as much money this year as last.” means how much profit or net income did Reliance Industries made

Let me ask you a question. Do we need money? If yes, for what? Well, we need money to:

• Buy things such as food, clothes, cars, CDs, books etc.

• To pay the maids, the milkman, drivers, doctors, to pay for school

fees etc.

• To go to restaurants, movies, travel etc.

Is Money Everything?

The stranger appeared again and asked if King was happy with his golden touch. The King said “No, I am the most miserable man on the earth.” He cried and asked for forgiveness. He said, “I will give up all my gold, please, please give my daughter back.” The stranger reversed the spell. King Midas got his daughter back.

Money can’t buy happiness. Money is important no doubt but one should not run after it at the cost of your study or health or relationships

.

“Money can be translated into the beauty of living, a support in misfortune, an education, or future security. It can also be translated into a source of bitterness,” said Sylvia Porter (1913–91) U.S. economist and journalist

Needs and Wants

- Kshitij was crying again. He wanted the Ben10 toy from McDonald Happy Meal. He already had two. He wanted the third one.

- Meghna had gone shopping with her mother to West Side. There she saw a new pair of jeans. She started pestering her mother, “Mummy I need these jeans. They are so cool, so rocking. I can wear this for Tanya’s birthday party.” Her mother tried explaining, “You already have so many of them, you don’t need another one.”

- Ishaan came running to her father, “Dad I need a sweater, its winter and my old sweater is no longer fitting me.” “Yes dear, we shall buy it when we go shopping this weekend.”

- Aryan had gone to watch a movie with his parents. Once the movie got over, he asked his parents, “Mummy, Papa I am hungry, I need to drink CocaCola.” “No,” his father said, “You don’t need CocaCola, what you need is a glass of water and some food like Dosa. Let’s go to the food court and take something from there.”

In all the above conversations, you saw that the kids are saying “I want,” “I need.” Let’s see what we really need for a living.

Aryan is hungry, he wants something to drink and eat. We need food to eat and if we do not eat food for long, we’ll become weak. Why do we need food? Cars are great to travel. We can go to far off places. But, a car needs petrol to run. Our body is a machine like a car, it too needs food to run well. If we don’t give petrol to the car, it will not run; if we don’t give food to the body, it will become weak. What if, instead of petrol, we put water in the car, will it run? No, right? As a human being, we have lots of choices in terms of food. There are different kinds of food, roti, subzi, rice, dal(pulses), eggs, vegetables, cheese, butter, dosa, idli, pasta, noodles, french fries, pizza. While French fries, Maggi is tasty, they are not healthy and do not provide us with the nutrients we need. We need to eat a balanced diet. What about eating ice cream? Ice creams are so tasty, I love having them. But then, I don’t have to eat it to live. It’s a different matter whether you eat in a five-star restaurant or eat roti and onion. Cola tastes good. Drinking a Fanta or Pepsi makes us feel good. But we don’t need the soft drink to survive. Water is good. It is said that we should drink at least 8 glasses of water every day. Milk and juice have calcium, vitamins and minerals that our body needs. So, Aryan’s father was right. Aryan can drink water and then eat Dosa or McDonald burger. Ice cream maybe.

Meghna wanted to buy a new pair of jeans and Ishaan, a new sweater. We need clothes to cover our bodies, to protect it from heat and rain. We wear clothes according to the season. In summers, we wear bright cotton clothes while in winter we wear woollen clothes. How many clothes can we wear at one time? Only one dress, right? Meghna has many jeans; one more jeans would fill her cupboard, but even if she does not buy it, that is okay. She can survive. Ishaan has to have a sweater. If he does not get one, he might fall sick and miss his school.

And Kshitij asking for McDonald toy was a want and not a need.

Did you see the difference between want and need?

Needs are things that we cannot live without. They are essential for us, such as:

• Food

• Place to live

• Clothes

• School

• Transportation.

Wants are things that we desire now, at that moment. Right now one wants a new pair of jeans; when one sees a new pencil box, one wants it. There is no limit to our wants. When a want is fulfilled, another one will come up. It is great to have other jeans but one can live without it, just as one can live without things such as:

• That dress like Barbie.

• Toys

• Chocolates

• Video games

Need-Want Quiz

1) Is house a need or a want?

2) Is car a need or a want?

3) What about a IPad? Want or need?

4) How about medicine? Want or need?

5) What about school? Want or need?

How do People Earn?

There are many ways in which people earn. Robert Kiyosaki author of Rich Dad Poor Dad book classified way people earn money into 4 categories: Employee Business owner Self-employed worker Investor.

• Employee: Employees earn income by working for other people. Most individuals are in this area. One works for a company and trades his time for money. If one wants to earn more money, one must work more hours. Another option is work for another company that pays better. If you don’t work, you don’t make any money.

• Self-employed worker: Self-employed people earn income by working for themselves – they own their jobs. This quadrant includes Doctors, Lawyers, Accountants etc. etc. highly specialized individuals that are paid hourly rates. The disadvantage if they are sick then income stops.

• Business owner: Business owners earn income from the businesses they own. They have others working for you as employees. They aren’t selling time for money, but rather selling a product or service

• Investor: Investors earn income from their investments – from money generating more money.

The rules of the game are totally different in each quadrant. They are completely different worlds and require different mindsets, tools, skills and behaviour.

Traditional schooling teaches us largely to focus on becoming an Employee (E) or a high-paid Self-Employed(S) individual such as a doctor, lawyer or accountant. You should follow Continuous learning and education in order to help you on this journey through each quadrant.

Credit Cards and Debit Cards

You would have often seen people using cards in shops. They buy things, at the counter they give a card to shopkeeper who swipes the card on a machine, gives a receipt and people walk off with their things without paying any money seemingly. These cards can be a debit card or credit cards generally called plastic cards. The plastic cards are an inevitable part of our lives. Plastic cards are one of the most popular forms of payment. They allow users to pay for goods and services easily and conveniently, virtually anywhere in the world, hence providing a secure alternative to cash and cheques

There are two kinds of Plastic cards, which are used to buy goods and services.

- Debit Card: On using a debit card, the money is immediately deducted directly from the user’s The user can buy things as long as there is money in his account. A debit card is a way to “pay now.”

- Credit Card: Here, the person uses the card to buy and then pays back later. There is a limit to which one can buy on credit card.

What happens when a credit card is swiped?

Mr Kumar wants to buy a TV using ICICI credit card (a MasterCard ). The shopkeeper at Sony Showroom swipes the ICICI credit card on a machine provided by a bank, say UTI bank.

Let’s look at the formal definition of people involved.

- Cardholder: An individual to whom a credit card is issued. Typically, this individual is also responsible for payment of all charges made to that card.

- Card Issuer: An institution, that issues credit cards to cardholders. This institution is also responsible for billing the cardholder for charges.

- Card Acceptor or Merchant: The individual or business accepting credit card payments for products or services sold to the cardholder. Merchant is also called Card Acceptor.

- Acquirer: An organization that collects (acquires) credit authorization requests from Card Acceptors and provides guarantees of payment. The merchant swipes the card on the acquirer’s swipe machine. He submits all the signed slips to the acquirer and collects payments from the acquirer.

- Credit Card association: An association of card-issuing banks such as Visa, MasterCard, Rupay etc. that set transaction terms for merchants, card-issuing banks, and acquiring banks

In the stated example, Mr Kumar is the cardholder; ICICI bank is the card issuer; the merchant is the shop: here Sony Showroom and UTI Bank is the acquirer and MasterCard is the card association.

- When the merchant/shopkeeper at Sony World, swipes Mr Kumar’s ICICI credit card on a machine provided by the UTI bank, the machine dials a stored telephone number via a modem to call the acquirer bank: UTI bank in this example. Details of purchase, such as, Cardholder name, number, date of expiry of the card, amount of money that Mr Kumar has to pay and merchant id, are sent to the UTI Bank

- The acquirer, UTI bank contacts ICICI bank through MasterCard network. It asks for the validity of the credit card and the credit limit. Firstly, ICICI card checks the validity of the credit card. If the card is valid, it also checks the transaction amount with the available credit limit. Based on that, ICICI Card approves or rejects the transaction.

If ICICI bank approves the transaction, a credit card transaction receipt is printed by UTI bank machine. Mr Kumar signs the receipt and gives it to the merchant. The signed receipt is like a promise made by Mr Kumar to pay the money to ICICI bank. The merchant gives one copy of credit card receipt to Mr Kumar and saves the signed receipt with him.

For using the swiping machine of UTI bank, the merchant will have to pay UTI bank a Merchant Discount Fee.

- When the shopkeeper submits such receipts to UTI bank, UTI bank pays the amount due to merchant including the Rs 20,000 owed by Mr Kumar after deducting the Merchant Discount Fee. For example, if Merchant Discount Fee is 2% then UTI bank will deduct 2% of Rs 20,000 = Rs. 400 and give Rs.19600 to the merchant.

At some shops, the merchant asks the customer to pay the merchant discount fee if paying by credit card.

- UTI bank will send the transaction details to ICICI bank through MasterCard interchange. ICICI Bank will pay the amount to UTI bank after deducting the Interchange transaction fee. Interchange transaction fee is a fee paid by an acquirer,,UTI bank in this example, to the issuer of the credit card, ICICI Bank in this example. In the example, let interchange transaction fee be 1%. So, ICICI bank will deduct 1% of 20,000 = Rs 200 and pay Rs 19800 to UTI Bank.

- ICICI bank will send the credit card statement to Mr. Kumar. Mr. Kumar will then repay Rs 20,000 to ICICI bank.

When Mr. Kumar used the credit card to pay, then:

- ICICI bank earned Rs 200

- UTI bank paid Rs 19600 to the merchant and got Rs 19800; so it also earned Rs 200. Merchant had to pay Rs 400.

- Mr. Kumar got the TV he wanted and paid Rs 20,000.

The image shows the various steps in one credit card transaction.

Rich and Poor Countries

Which are the rich countries in the world? Which are the poor countries and why are they poor?

How many countries are there in the world? There are between 168 and 254 nations, depending on who is doing the counting.

- As on May 1, 2008, the United Nations has 192 members.

- The US State Department recognizes 195 independent countries around the world.

- Most of the current World Almanacs use 193 countries. The political world is constantly changing.

There are approximately 170 separate currencies, 239 two-letter country codes recognized by the ISO (International Standards Org.), and the Universal Postal Union has listings for 500,000 localities in 189 Countries.

Which are the rich countries in the world?

The question is how does one measure the money in a country?

Experts have come up with ways to define what a rich country is. Some experts say that value of all final goods and services produced in a country in one year is to be used as a measure, called Gross Domestic Product (GDP); while other experts say that value of all goods and services produced in a country in one year by the nationals, plus income earned by its citizens abroad, minus income earned by foreigners in the country should be used as a measure, called Gross National Product (GNP).

Different international financial institutions have been set up. Some of these are:

- The International Monetary Fund (IMF): IMF is an organization of 189 countries, working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty around the world. (http://imf.org/)

- The World Bank: provides financial and technical assistance to developing countries for development programs (e.g. bridges, roads, schools, etc.) with the stated goal of reducing poverty. (worldbank.org)

- The United Nations (UN) is an intergovernmental organization tasked to promote international co-operation, to create and maintain international order, promoting human rights, fostering social and economic development, protecting the environment, and providing humanitarian aid in cases of famine, natural disaster, and armed conflict.

Model United Nations, also known as MUN, is an activity in which students can learn about diplomacy, international relations, and the United Nations. It is a way to become an active, more concerned global citizen, while in this era of globalization, being globally aware is more important than ever. MUN is an exercise in research, public speaking, and teamwork. MUN builds confidence and leadership and diplomatic skills.

Developed, Developing Countries

Countries are often loosely placed into the following categories of development:

- Developed countries: Canada, United States, European Union members, Japan, Israel, Australia, etc.

- Countries with an economy consistently and fairly strongly developing over a longer period : China, India, Brazil, South Africa, Costa Rica, Mexico, Egypt, much of South America, etc.

- Countries with a patchy record of development :most countries in Africa, Central America, and the Caribbean excepting Jamaica

The often used term “Third World” today mostly refers to underdeveloped or better developing countries.

The wealth of Countries based on GDP

These agencies come up with different ways to define rich countries.

As per International Monetary Fund(IMF) based on gross domestic product per capita at nominal values, the value of all final goods and services produced within a nation in a given year, converted at market exchange rates to current U.S. dollars, divided by the average (or mid-year) population for the same year. As per the IMF and the GDP per capita, the world looks as follows:

India’s rank

- As per IMF: 142 with GDP of $ 1,723 in 2016

- As per WB:134 with GDP of $ 1,709 in 2015

- As per United Nations: 147 with GDP of $ 1,614 in February 2015

Banks in India

Just as the teachers and students in a school are supervised by a Principal, similarly all the banks of a country are supervised by the Central Bank. Central Bank of India is the Reserve Bank of India (RBI). Reserve Bank of India (RBI) is the central bank of the country and is different from Central Bank of India. Some of the central banks of other countries are as follows:

- United States – Federal Reserve System

- The European Central Bank is the central bank for the euro and administers monetary policy of the eurozone, which consists of 19 EU member states and is one of the largest currency areas in the world.

- United Kingdom: Bank of England

- Australia: Reserve Bank of Australia

- China (Mainland) – People’s Bank of China

Reserve Bank of India

The RBI is the supreme monetary and banking authority in the country and controls the banking system in India. RBI issues the bank notes & also checks that all the banks are working properly. It is called the Reserve Bank’ as it keeps the reserves of all commercial banks.

- It is issuer of currency. Our notes are signed by Governor of Reserve Bank of India.

- Acts as the Banking regulator : It lays down rules and regulations for various banking activities such as loan, credit cards or debit cards

- Manages the Foreign Exchange

- Acts as the banker to the Government.

Types of Banks

One way to classify it as Public sector banks, Private Sector Banks, Foreign banks etc.

- Public sector banks or PSU- for example: State Bank of India, Bank of India, Punjab National Bank etc. Public sector banks are those which are operated by government bodies.

- Private sector banks for example: ICICI Bank, HDFC Bank, ING Vysya Bank. Private sector banks are the banks which are controlled by the private lenders with the approval from the RBI.

- Foreign banks for example: HSBC, Deutsche Bank. These banks offer banking services but are actually branches of banks of other countries, for example, HSBC is Hong Kong and Shanghai Banking Corporation. It is headquartered in England and is Europe’s biggest bank

Commercial banks are the most important types of banks. The term ‘commercial’ carries the significance that banking is a business like any other business. In other words, commercial banks are essentially profit-making institutions. They collect deposits from the public and lend money to business firms (manufacturers), traders, farmers and consumers. Generally, the term ‘banks’ to refer to commercial banks.

Payments bank is a new model of banks conceptualised by the Reserve Bank of India (RBI). These banks can accept a restricted deposit, which is currently limited to ₹1 lakh per customer. Payments banks can issue services like ATM cards, debit cards, net-banking and mobile-banking. These banks cannot issue loans and credit cards. Both current account and savings accounts can be operated by such banks.

If you don’t teach your kids how to manage money, somebody else will. Is that a risk you want to take? Teach your kids how to handle money now, and they won’t end up with money regrets later on in life. You can give them the head start you wish you’d had.

Lets Learn About Money bemoneyaware Book front cover

Buy from Amazon by clicking here

Buy from Flipkart by clicking here

If you don’t teach your kids how to manage money, somebody else will. Is that a risk you want to take? Teach your kids how to handle money now, and they won’t end up with money regrets later on in life. You can give them the head start you wish you’d had.