The Cost Inflation Index for FY 2023-24(AY 2023-24) is 348. This article gives Cost Of Inflation Index to be used from 1 Apr 2017 for calculating Long Term Capital Gain on Sale of real estate, unlisted shares, gold. It also gives an overview of Indexation and Long Term Capital Gains. Also Note, From April 1, 2023, investors in debt mutual funds, exchange-traded funds (ETFs), international funds, gold funds, and certain categories of hybrid funds will no longer enjoy the long-term capital gains (LTCG) tax benefits and indexation benefits.

The Cost Inflation Index for FY 2023-24(AY 2023-24) is 348

The Cost Inflation Index for FY 2022-23 relevant to AY 2023-24 is 331.

Cost Inflation Index or CII for the Financial Year 2021-22 was 317

Table of Contents

Cost of Inflation Index till FY 2023-24

Indexation adjusts the purchase price of an asset based on inflation during the investment period, which can reduce tax liability.

| Financial Year(FY) | Assessment Year(AY) | Cost Inflation Index |

| 2001-02 | 2002-03 | 100 |

| 2002-03 | 2003-04 | 105 |

| 2003-04 | 2004-05 | 109 |

| 2004-05 | 2005-06 | 113 |

| 2005-06 | 2006-07 | 117 |

| 2006-07 | 2007-08 | 122 |

| 2007-08 | 2008-09 | 129 |

| 2008-09 | 2009-10 | 137 |

| 2009-10 | 2010-11 | 148 |

| 2010-11 | 2011-12 | 167 |

| 2011-12 | 2012-13 | 184 |

| 2012-13 | 2013-14 | 200 |

| 2013-14 | 2014-15 | 220 |

| 2014-15 | 2015-16 | 240 |

| 2015-16 | 2016-17 | 254 |

| 2016-17 | 2017-18 | 264 |

| 2017-18 | 2018-19 | 272 |

| 2018-19 | 2019-20 | 280 |

| 2019-20 | 2020-21 | 289 |

| 2020-21 | 2021-22 | 301 |

| 2021-22 | 2022-23 | 317 |

| 2022-23 | 2023-24 | 331 |

| 2023-24 | 2024-25 | 348 |

Indexation and Tax on Long Term Capital Gains

Indexation refers to the adjustment in the purchase price of an investment for the inflation rate during the period for which it was held. This inflated cost is considered as the purchase price while computing the gains arising from the sale of the asset from the taxation perspective. When you sell property, gold, shares, mutual funds, you need to pay capital gain. If the holding period of asset i.e time between sale and purchase of the asset is more than 2 years for property and more than 3 years for unlisted shares, gold, and debt funds then one uses Cost of Inflation Index for calculating Long Term Capital Gains (LTCG) to reduce the tax.

Note: From April 1, 2023 Long term capital gains made on debt mutual funds, exchange-traded funds (ETFs), international funds, gold funds, and certain categories of hybrid funds, will no longer enjoy the indexation benefits. The new tax law is applicable only to those mutual fund schemes whose weight in equity or stocks is less than 35%. Explained in detail below

The formula for calculating the new Purchase price using Cost of Inflation Index is as below.

Indexed Cost of Acquisition=(Cost of Acquisition * Cost of the Inflation Index (CII) for the year in which the asset was sold or transferred.)/ The cost of Inflation Index (CII) for the year in which the asset was first held by the assessee OR FY 2001-02, whichever is later.

Let’s see the how the indexed cost of acquisition will be calculated using Cost of Inflation Index or CII. If Shyam purchased the property in FY 2005-06 at Rs.80 lakh when Cost of Inflation Index or CII is 117 and sold the same in FY 2017-18 at Rs.1.5 Cr when Inflation Index or CII is 272.

However, if Shyam does not consider the indexed cost, then the gain would be as Rs.90 lakh (Rs.1.5 Cr-Rs.60 Lakh).

But as Shyam has held the property for more than 2 years, he can use Cost Inflation Index to bring down the tax. So the new purchase price taking care of inflation using Cost of Inflation Index or CII is

Indexed Cost of Acquisition or Purchase Price =(60,00,000 * 272)/117=Rs.1,39,48,717.95. (Around 1.39 crores)

So the Long Term Capital Gain=Selling Price-Indexed Cost of buying property=1.5 crore – 1,39,48,717.95 = 10,51,282.05 (around 10.5 lakh)

No Indexation benefits from April 1, 2023 on Mutual Funds

From April 1, 2023 Long term capital gains made on debt mutual funds, exchange-traded funds (ETFs), international funds, gold funds, and certain categories of hybrid funds, will no longer enjoy the indexation benefits. The new tax law is applicable only to those mutual fund schemes whose weight in equity or stocks is less than 35%.

But the investors who had bought such funds before 01-Apr-2023 would continue to enjoy the old LTCG rule with indexation benefits. The new taxation system is applicable only on purchases made on or after 01-Apr’2023

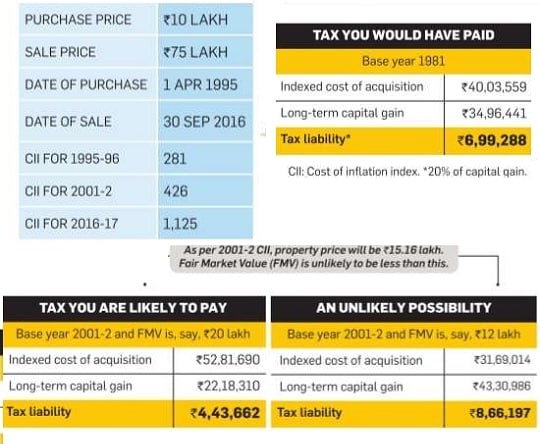

Base Year for Calculation of Capital Gains

Change of Base Year from 1981 to 2001 impact on Capital Gains

Overview of Capital Gain Tax on Sale of House or Property

Our article How to Calculate Capital gain Tax on Sale of House or property? explains it in detail.

- The time period: Check the time period between when you bought the house/property and when you sold it. if you have inherited the property the period of holding will be considered from the date of purchase by your ancestors.

- If a property is sold within two years(from FY 2017-18 earlier was three) of buying it, it is treated as a short-term capital gain. This is added to the total income and taxed according to the slab rate.

- If a property is sold after two years (from FY 2017-18 earlier was three) years from the date of purchase, the profit is treated as a long-term capital gain(LTCG) and is taxed at 20% after indexation.

- The Purchase cost and Fair Market Value: If the property is purchased before 1 Apr 2001 then the fair market value of the property as on 1 April 2001 can be considered as the cost of acquisition. For ascertaining the Fair market value, it is best to engage the services of a registered valuer. Our article Fair Market Value: Calculating Capital Gain for property purchased before 2001 covers it in detail

- House improvement cost and transfer cost: While computing the cost of acquisition one can also add the costs incurred with respect to procedures associated with house improvement or transfer cost such as the will and inheritance, obtaining succession certificate, costs of the executor, property valuer etc.

- Find the indexation purchase cost: The long-term capital gain(LTCG) shall be computed as the difference between net sale proceeds and indexed cost of purchase. For indexation, the cost of acquisition should be adjusted by applying the cost inflation index (CII).

- Find the capital gain. Check out our Capital Gain Calculator from FY 2017-18 with CII from 2001-2002

- For short-term capital gain = final sale price – (the cost of acquisition + house improvement cost + transfer cost).

- In case of long-term capital gain, capital gain = final sale price – (transfer cost + indexed acquisition cost + indexed house improvement cost).

- Saving Long Term Capital Gain: If there are any long-term capital gains, one may have to either

- Pay tax on it at the rate of 20% OR

- Buy House OR

- 1 year before the sale or

- 2 years after the sale of the property/asset OR

- Construct a new residential house property must be constructed within 3 years of the sale of the property.

- Save capital gains tax by buying specified bonds under Capital Gain Account under section 54EC before filing Income Tax Return for that year. Our article Capital Gains Account Scheme and Sale of property explains it in detail.

- Capital Loss: Set off of Capital Losses: The Income Tax does not allow Loss under the head Capital Gains to be set off against any income from other heads – this can be only set off within the ‘Capital Gains’ head. Our article Capital Loss on Sale of House discusses it in detail.

- Long-Term Capital Loss can be set off only against Long Term Capital Gains.

- Short-Term Capital Losses are allowed to be set off against both Long-Term Gains and Short Term Gains.

- Carry Forward of Losses if the return is filed before due date: If you are not able to set off your entire capital loss in the same year, both Short Term and Long Term loss can be carried forward for 8 Assessment Years immediately following the Assessment Year in which the loss was first computed. To keep a track of your losses, the Income Tax Department has laid out that Losses for a year cannot be carried forward unless that year’s return has been filed before the due date. Even if it’s a loss return, you do not have any income to show – do file your return before the due date.

How to determine the cost of acquisition of the Flat purchase. I have 2 agreements. 1: A formal agreement (stamp paper of 100 Rupees ) between builder and myself, 2: A register sale deed . In both of the agreement I have two different amount. Not sure how to calculate the the Cost of Acquisition.

sir,

a flat purchased for 165000/- in 1993( possession with full payment) and registered agreement in 2016 and now being sold for 24,25,000/- in oct 2017. please guide what will be minimum tax liability on capital gain after indexation benefit. Also advise if costs paid on maintenance of plot from 2001 onwards for 350000/- & purchase registered agreement(2016)for 200000/- & transferred brokerage cost 55000/- can be included in cost of acquisition and any tax benefit be derived out of it. please help me.

Hi,

My father who is 60 years old now had an inherited land for which the paper works shows 5000Rs dated 30th Jan 1995, He built a house on it during 2007. Now he sold the land with house for 3000000 on 30th Jan 2018 with a sale agreement of 1800000. How much capital gain tax will be applicable on this 3000000?

I HAD PURCHASED A PLOT IN 1,85,000/- IN 1997. NOW I HAVE SOLD THAT IN 7,00,000/- IN JUNE 2017. PLEASE INFORM ME HOW MUCH IS THE LONG TERM CAPITAL GAIN AND WHAT TAX LIABILITIES I HAVE TO BEAR.

Sir From 1 Apr 2017 base year to be used for indexation has changed from 1981 to 2001.

So you need fair market value as on 1 Apr 2001. Our article Fair Market Value: Calculating Capital Gain for property purchased before 2001 explains it in detail.

Assuming the price as 1,85,000 in 2001, calculations are shown below

Investment Type:Real Estate

Time between: 16 years 65 days

Gain Type: Long Term Capital Gain

Difference between sale and purchase price: 515000

CII of the Purchase Year: 2001 month: Apr : 100

CII of the Sale Year: 2017 month: Jun: 272

Purchase Indexed Cost:503200

Difference between sale and indexed purchase price: 196800

Long Term Capital Gain Tax with indexation (at 20%):39360

I have purchase flat in Mumbai in 1997 for Rs 4.6Lacs .

I will be selling in 2018 Oct for Rs 80 Lacs.

1) Have I to get fair value as on Yr 2000 from govt. Valuer & Add in index of 270 % on his value to arrive at cost of acquisition?

If I have no or less than the taxable income in a particular year do I still pay tax on my longterm capital gain obtained through my investment in debt funds

No you don’t have to pay is you are a resident Indian.

But whether you have to file ITR is a separate question which has to decided based on whether you filing ITRs earlier,

whether you need to take a loan/visa.

A resident individual/HUF can adjust the exemption limit against LTCG.

For example

Mr. Kapoor (age 67 years and resident) is a retired person. He purchased a piece of land

in December, 2010 and sold the same in April, 2016. Taxable long-term capital gain on

such sale amounted to Rs. 1,84,000. Apart from gain on sale of land, he is not having any

other income. What will be his tax liability for the year 2016-17?

For resident individual of the age of 60 years and above but below 80 years, the basic

exemption limit is Rs. 3,00,000. Further, a resident individual can adjust the basic

exemption limit against LTCG. In this case, LTCG of Rs. 1,84,000 can be adjusted

against the basic exemption limit. In other words, Mr. Kapoor can adjust the LTCG on

sale of land against the basic exemption limit.

Considering the above discussion, the tax liability of Mr. Kapoor for the year 2016-17

will be nil.

I have sold residence flat on July 2017. (Purchase on 2007)But i don’t want to purchase the property now.so I want to deposit capital gain amount to Long term capital gain Account 1988. to save long term capital gain tax.for that I want full detail . When I should open account up to what time I should deposit amount etc.

Our article Capital Gains Account Scheme and Sale of property explains it in detail.

If one is unable to buy the benefit Before due date of filing of Income Tax Returns for that year one has to open a Capital Gains scheme account with any scheduled bank in order to convince the government that he intends to invest the so earned capital gain in some array but needs some more time to do so.

So for property sold in Jan 2018 if he has not bought a house till 31 Jul 2018 then he needs to open Capital Gains scheme account.

Note: If you deposit the capital gain not utilized after the last date of filing ITR (5 Aug 2018) then the capital gain amount will not be eligible for exemption under section 54 under any circumstances. You need to pay Long-term capital gain (LTCG) tax of 20% on the amount.

OFFHAND (To share own thoughts as shared before, out of sheer empathy/compassion):

The change in ‘Base Year’ , has, as largely observed, been a matter of most concern to those holding an asset squired at any point in time, before the cut-off year of FY 2001-02, transfer of which is /likely to be made in FY 2017-18, or a later year.

And, in one’s perspective, founded on a conjoint and harmonious reading – mindful study and incisive understanding- of the amended provisions, taxpayer will have a good case to strongly urge /contest that, – the cost of acquisition of such asset should be taken into account at its indexed cost, – also, as its ‘FMV’ – arrived at by applying the CII as laid down in the old Table (in force for and up to FY 2016-17).

May add that, a personal feedback- input sent through the website of the Department, seeking clarity, has, so far as known, remained to be taken a note of and left to be clarified.

For MORE , look up the personal Posts , besides in other social websites, on FB/LInkedin.

Thanks for sharing

ir,

I have purchased a house,in HYDERABAD,(TELANGANA ) on 24 -01-2004 for

Rs 2000000/-(Rupees Twenty Lakhs only )& incurred an expenditure of Rs 600000/-

( Rupees Six lakhs only ) over a period of 13 years;

I have sold the said house for Rs 19000000/ ( Rupees One Crore and Ninety Lakhs only )on

06-01-2018

QUERY

1.WHAT IS THE AMOUNT OF CAPITAL GAINS TAX

2.WHAT ARE THE EXEMPTIONS

KR

I purchased a Residential Flat 2015 for 17.52 lakhs.

If I plan to sell it for 25 lakhs now (tentatively in Feb 2018) what is Capital Gain tax liability

Can I Purchase any residential PLOT/Land to exempt tax? If so, what is time limit to Invest after transfer.

When did you buy the property before 1 Apr 2015 or after 1 Apr 2015?

If you bought property After 1 Apr 2015 Long-Term Capital Gain Tax with indexation (at 20%):1,24,768.5.

Calculation for If you bought the property before 1 Apr 2015 are shown below

Investment Type:Real Estate

Time between buying and selling is more than 2 years

Gain Type: Long Term Capital Gain

Difference between sale and purchase price: 748000

CII of the Purchase Year: 254

CII of the Sale Year: 272

Purchase Indexed Cost of 17.52 lakhs:1876157.48

Difference between sale and indexed purchase price: 623842.52

Long Term Capital Gain Tax with indexation (at 20%):124768.5

For property purchased before 1 Apr 2015 Long Term Capital Gain Tax with indexation (at 20%):1,02,880

CII of the Purchase Year: 201 240

CII of the Sale Year: 2017 month: Dec : 272

Purchase Indexed Cost:1985600

Difference between sale and indexed purchase price: 514400

Long Term Capital Gain Tax with indexation (at 20%):102880

The interest paid for housing loan from financial institution shall be eligible for aggregation to cost of working the calculation of indexed cost for income tax purposes.

I bought a flat in Rs. 860000.

Sale deed happened in Jan 2011. Registry done on April 2011.

Stamp duty paid Rs. 54910; Registry charges – Rs. 9100

Flat sold in Sept 17 in Rs. 150000.

How much Capital Tax i need to pay & how if i do not invest in reality.

What will be the year of purchase as per above for calculation.

Cost of inflation should be 223614 so I should pay tax of 20%of it that is 44722 other wise I can save tax by investing 223614 into the NHAI-REC bond for 3 years

I bought a flat in Sept 2001 for 10 lacs and sold in November 2017 for 42 lacs. I have spent renovations brokerage stamp duty etc around 15 lacs till date for old flat. What is cost of inflation from 2001 t0 2017 and how much I need to pay capital gain tax if not interested in bonds or property

DEAR SIR,

I WAS ALLOTED A RESIDENTIAL PLOT IN 2006 BY PUDA. THE PAYMENT SCHEDULE INCLUDED APPLICATION MONEY IN 2005, ALLOTMENT MONEY IN 2006 AND 6 ANNUALEQUAL INSTALMENTS

WITH FINAL INSTALMENT / PAYMENT MADE ON 2012.

FOR CALCULATING THE INDEXED COST , WILL 2006 BE THE BASE YEAR OR 2012.

Sir, I have purchased a residential flat in Kolkata for 7 lakhs in 2008-09 and want to sell it now at Rs 25 lakhs now (2017-18). Calculation of long term capital gain, as per your formula is 25 – 7*272/137 = Rs 11 lalks. Kindly confirm the calculation.

Also can I avoid paying the Long term capital gains by investing in any capital bond under Section 54EC of the Income-Tax Act ?

Hello,

We had land in the name of family 7 heirs (purchased for approx. Rs. 20,000 in 1968).

We have entered into development contract in Feb-2004 with a builder. At the time of contract my share works out to market value Rs, 17,11,928 (value of land as per challan for contract reg.)

I got possession of flat in Aug 2010 (free of cost) but market value is Rs. 460,500 (as per challan for contract reg.).

Now, I sold flat in Sep-2017 for Rs. 79,00,000. Can you tell me what is my LTCG?

Is it to be calculated basis (1) value of land in Feb-2004 or (2) value of flat in Aug-2010?

As per (2) value of flat in Aug-2010, ICOA = (460,500 / 167) * 272 = 7,50,035. LTCG = 79 lacs – 7.5 lacs = 71.5 lacs.

Is this correct?

Sir I don’t think that a land acquisition by will or gift is under the head of CG .

In year 1990-91 my father purchased flat for Rs 1,30,000. He is selling it this month Oct 2017 for RS 24,60,000. What’s the tax he will incur.

Dear sir, I bought a flat in FY 2012-13 for which total cost of acquisitions including stamp duty registration and brokerage is 1907680. I sold the same flat in September 2017 at 40 lakhs. Brokerage extra I paid 48,000. Please let me know my capital gains tax. And also suggest how to avoid taxes.

I have following queries :-

1) Cost of acquisition of property will be registered value or registered value+registration charges plus freehold charges+brokerage(if receipt of broker is there).

Dear Sir,

I’m taking a quick example to confirm my understanding on this topic – The example that I took here is that a flat was bought and registered in 2007 and sold in 2017. Is below calculation accurate and are construction and stamp duty/ reg charges included in total cost of acquisition?

Undivided Land Price/ Sale Deed Value – A Rs. 1,00,000

Flat Construction Price per Construction Agreement Between Buyer and Builder – B Rs. 20,00,000

Stamp Duty/ Registration etc. – C Rs. 1,00,000

Cost Inflation Index during FY 2006-07 -D 122

Cost Inflation Index during FY 2017-18 – E 272

Purchase Price (A+B+C) Rs. 22,00,000

Indexed Cost of Acquisition or Purchase Price = (Purchase Value x Cost Rs. 49,04,918

Inflation Index during 2017-18 – E)/Cost Inflation Index during 2006-07 -D

Sale Price Rs. 25,00,000

Long Term Capital Gain = Sale Price – Indexed Cost of Acquisition or Purchase Price -Rs. 24,04,918

Appreciate your early response on it.

Regards,

Nez

If you bought your property between 1 Apr 2006 and 31 Mar 2007 then you can use CII of the FY 2006-07.

Then your calculations are correct. You can verify it using our Capital Gain Calculator

So you have a capital loss

if there is a net loss under the head Capital Gains for an assessment year, the same cannot be set off against any other head of income viz., Salaries, House Property, Business or Profession or other sources. It has to be separated into Short term Capital Loss (STCL) and long term capital loss (LTCL). Our article Capital Loss on Sale of House discusses it in detail

Sir,

I have sold two residential flats in this financial year 2017-18 (flat ‘A’ acquired in 1999-2000, flat ‘B’ acquired in 2009-2010). After adjusting for CII, there is a long term capital gain of Rs. 20 lakh on sale of flat ‘A’, and loss of Rs.22 lakh on sale of flat ‘B’. Will LTCG from flat ‘A’ get offset against loss from flat ‘B’ in this case? Or will LTCG from flat ‘A’ be treated separately?

Yes you can Club the gains or losses from the sale of two houses. So your total capital gain or loss would be sum of gain of 20 lakh and loss of 22 lakh so net effect is loss of 2 lakhs.

I appreciate the quick response. Thanks a lot.

SECTION 48 OF THE INCOME-TAX ACT, 1961 – CAPITAL GAINS – COMPUTATION OF – NOTIFIED COST INFLATION INDEX UNDER SECTION 48, EXPLANATION (V) – FINANCIAL YEAR 2017-18

NOTIFICATION NO. SO 1790(E)[NO. 44/2017 (F. NO. 370142/11/2017-TPL)], DATED 5-6-2017

As per the above notification, the new CII of 272 for PY2017-18 will become applicable from April 1, 2018.

My doubt is if it is meant for PY2017-18, the effective should be April 1, 2017 and not April 1, 2018. Please clarify my doubt.

You are right. It is effective from 1 Apr 2017.

sir

i inherited a property in 1997 consisting of a building and a factory,i stopped the factory in 1999 and in 2000 converted the building into a hotel spending about 30 lakhs ,out of which 25 lakhs was loan ,the entire loan has been repaid and i intent to dispose the property ,i have been offerd 20 cr for the property,how much will be the tax liabilty,and how can i save tax

For the purposes of calculating capital gains on properties before 2001, you have to know the fair market value (FMV) of a property in 2001.

According to the Income-tax Act, 1961, fair market value is the price that the capital asset would ordinarily sell in the open market on the relevant date.

According to the Income-tax Act, 1961, FMV shall be the higher of

—cost of acquisition of the property, or

—the price that the property shall ordinarily sell for if sold in the open market.

However, “There is no fixed formula to calculate FMV of a property. The technique most widely used to estimate FMV is to look at the sale instances of similar properties in the same neighbourhood. The other option is to look at circle rates

Calculating the LTCG based on any arbitrary FMV can land an assessee in trouble, if the assessing officer (AO) has a different opinion or doubt over the declared value

It is advisable to get the valuation of the property done from the registered valuer.

Government-approved valuers follow a standard process for the valuation and provide a detailed report. In addition to other parameters “to derive at the FMV of a property, a valuer also considers area and dimensions of the property, is it freehold or leasehold, is there any restrictive covenant in regard to use of such property, insurance of the land and property, if the land falls under any development plan of the government

A valuer needs to be registered under section 34AB of Wealth Tax Act, 1957, to act as a recognized valuer of income tax department,” said Bansal. Each valuer is provided with a license from the department to work as a valuer. Fee and charges that a valuer can charge are also prescribed under the Act, and depend on the value of an asset. For instance, for first the Rs5 lakh of asset value, fee would be 0.50% of the value. For next Rs10 lakh, it would be 0.20%, for next Rs40 lakh 0.10% and 0.05% of the value thereafter. Typically, a valuer takes 3 to 4 days to prepare a valuation report

In case and AO raises any doubt over the report it is valuer responsibility to reply, and if needed, the valuer can even visit the AO for clarification on the report

An assessee should keep the valuation report along with other documents related to capital gains, for at least 8 years after the relevant assessment year.

The site purchased at around Rs.1.00 lakh (Cost of site+Stamp duty brokerage etc) during Oct 2003 was sold last month at around 40,00,000/-(cost excluding Brokerage Stamp Duty and NOC charges etc). Please let me know the amount of Capital Gain in the transaction and what will be the LTCG tax to be paid if Gain is INDEXED or NOT INDEXED

for AY 2018-19. As there is no intention of reinvesting in any property please guide me whether it is worth paying out the tax OR investing in in REC or NHAI bonds.

Capital Gain Calculation is as follows:

Time between :14 years 4 days

Gain Type: Long Term Capital Gain

Difference betweem sale and purchase price: 3900000

CII of the Purchase Year: 2003 month: Apr : 109

CII of the Sale Year: 2017 month: Apr : 272

Purchase Indexed Cost:249541.28

Difference between sale and indexed purchase price: 3750458.72

Long Term Capital Gain Tax with indexation (at 20%):750091.74

It depends on whether you need the money or not? And for how long.

I purchased a plot of land for Rs.5000/ in the year 2001 and constructed house in 2002 at the cost of 115000. I spent 30000 for furniture in 2007-08. I have no bills. I sold the house in July,2017 for 59000. What will be my capital gain tax?

My son bought a residential property in October 2004 and spent a few lakhs of Rupees on upgrading the property with furnishings etc over the period of 4 years.

In March 2016, he gifted the property to me through a properly registered gift deed.

If I opt to sell the property during the FY 2017-2018, how do I calculate the Long Term Capital Gains Tax ?

Purchase Price & Purchase Date would be of original buyer Oct 2004.

Selling Price and Selling Date would be whenever you sell in FY 2017-18.

If you or your son have bills for upgrading the property then you can claim it as expenses.

My mother purchased a house in 2004 for 5.2L (including stamp and other expenses), sold it for 21 L in April 2016. Purchased a new house in 2016 for 35 L. Took a loan of 13 L and arranged rest amount from our side.

The house is in the name of my mother and myself, I pay loan EMI from my salary. Will get the house registered soon in our name in next 3-4 months.

Will I get an exemption on LTCG under section 54 of IT act?

If not will I attract LTCG?

Thank you.

Regards

Himanshu

i dont have any other source of income. i am not submitting income tax returns till now. I have PAN. I bought a house at 15 lakhs in March 2013 and selling it at 22 lakhs in August 2017.

Full value consideration is 22 lakhs

indexed value of acquisition is 15 x 272/200 = 20.4 lakhs

LTCG = 1.8 lakhs.

a) However this is less than the taxable exemption limit of 2.5 lakhs (i am a senior citizen, will it be3.0 lakhs?) , i need not pay LTCG is my understanding.

b) Do i need to submit IT return in June 2018 with the above information?

c) Also i had spent 4 lakhs on POP ceiling etc. Can this be used as improvement, but i dont have the bills.

Please advise.

The Long term capital gain of Rs. 1.8 lakhs is NOT your annual income but PROFIT and is taxable irrespective of your annual income. You will have to pay the tax at 20% of 1.8 lakhs i.e. 36000/- and will also have to file the IT returns. Unbilled expenses may not be allowed.

I

I have purchased property ( land) in 1981 and have sold it on 30/05/ 2017. Now with change in the base year as 2001 for CII how do I arrive at the market value of this property? My purchase value is Rs 2960/- and sale value is 232000/- What will be my indexed value for plot of land purchased at Rs. 2960/-.

Please help me, thanks.

A plot purchased for 110000 in 2001 and now being sold for 14 lac in July 2017 please guide what will be tax liability on capital gain after indexation benefit. Also advise if costs paid on maintenance of plot from 2001 onward for 235000 can be included in cost of acquisition and any tax benefit be derived out of it.