Companies often reward their employees with their stock, either in the form of employee stock option plans (ESOP) or Restricted Stock Units(RSU), or employee stock purchase plans (ESPP). Under the Employee stock purchase plan or ESPP, the employee has the choice of purchasing stocks of his company listed on the Stock exchange from his salary usually at a discounted price This article explains in detail ESPP. What is ESPP? Terms associated with ESPP, Tax Implications of ESPP, hot to calculate Long term capital gain/short-term capital gain?

Table of Contents

What is ESPP?

Under the employee stock purchase plan or ESPP, the employee has the choice of purchasing stocks of his company listed on the Stock exchange from his salary usually at a discounted price. These are different from ESOP, RSU, explained later in the article.

If an employee enrolls in ESPP then he will contribute a fixed part of his salary, usually between 1 percent and 15 percent, for a fixed period of time say 6 months. At the end of the fixed period, the company will use this money to purchase the company’s stock at a discount to the price of the share.

For example, if your company offers an ESPP plan twice a year which you can opt for, one window opens is Jan-June (where you can join in Jan only) and the other is July to Dec (You can join in July only). So you will have to tell the company how much you want to contribute each month. If you choose it to be 10%, then 10% of your salary will be deducted for the ESPP plan. Now suppose a person chooses the Jan-June window for ESPP and he is contributing 10,000 a month for this, then in next 6 months, the company will deduct Rs 60,000 for his ESPP from his salary. In July company will buy shares for him at discount price. Process will again be repeated for July to Dec window.

The discounted price depends on the policy of the company. In some companies, the lower of the prevailing price at the beginning or the end of the ESPP period is taken as the base price. For example, If the price at the start of the period is Rs. 70 and at the end is Rs. 100, then the lower price i.e Rs. 70, is considered as the price of the stock. At this price, the company gives a discount. So A discount of 10% on the base price will mean that the employee can procure the stocks at the rate of Rs. 63 per share.

How does ESPP work?

After the purchase, the stocks are credited to one’s Demat account. Shares are deposited in the brokerage account of the country where your company is listed. For USA-based companies listed on NASDAQ, there are trading portals like E*Trade, Charles Schwab Corporation, etc.

Once the shares are bought for you, they are yours. They are treated just like any other shares you have bought. You can hold them for as long as you want, you get to decide when to sell the shares. There are no restrictions. They are yours even when you leave the company. Investment in ESPP is similar to an investment in stocks so it suffers from stock market volatility.

As the company is giving you a discount on the stock price this part of salary comes under perquisite and hence is taxed as per your tax slab. So if you are in the 30% tax slab then ESPP contribution will be taxed at 30.9%(include education cess etc). Perquisite is calculated on the difference between the Market price and the allotment price at the time of purchase.

So if you got 10 shares when the market price of the stock was $12 and you got at $8.5 then you would be taxed on 10* ($12-$8.5) = $35= Rs 35 * US Dollar conversion rate one the date of allotment. The employer will deduct tax as per your income slab. Hence your actual discount becomes ~10%. This would be deducted by your company as TDS and deposited to the Indian Government. It would also be reflected on your Form 12BA. Our article Understanding Form 12BA explains perquisite and salary in detail.

For ESPP of stocks listed on stock exchanges outside India, One needs to show shares received as ESPP/RSU/ESOP of MNC as Capital Asset in Schedule FA(Foreign Assets) of ITR

FAQ on ESPP

Why do the companies offer ESPP?

It is one of the ways to attract and retain employees. It is also thought of motivating employees as shareholders to maximize returns both for them and the company.

Once enrolled in ESPP can one stop it?

The ESPP plans allow flexibility in terms of stopping the plan or modifying the contribution levels during the enrolment period. Some allow employees to even suspend their enrolment even during the offering period. In such cases usually, no further deductions from salary will be made but for the amount deducted already, it will purchase shares on the share date. Each ESPP plan is unique so please check your plan document for details

What if the stock price of the company goes down?

The company does not have any obligation to compensate the employee if the share price goes down. Tough luck man.

Should one enroll for the company’s ESPP?

Such perks come with their own set of rewards and risks

Benefits of RSUs/ESOPs/ESPPs

You get to buy stocks of your company, at a lower price than the market price. If your company does well, its stock price increases, and you have the potential to earn high amounts and create enormous wealth.

Risks of RSUs/ESOPs/ESPPs

Like any other stock, the stock price is volatile and exposed to various risks such as economic risks, geopolitical risks, etc. There is also the possibility of the stock price not rising.

Terms associated with ESPP

Typical terms associated with ESPP are as follows:

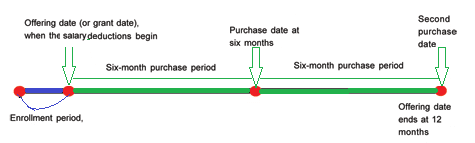

Enrolment Period: Period during which you can enroll for ESPP. If you miss this then you have to wait till the next enrolment period to get enrolled.

Offering Period: A period during which your salary gets deducted and accumulated for purchasing of company’s stock. It’s usually 6 months or multiples of 6 months. During the offering period.

Purchase Period: The purchase period is one after which the stocks will be purchased. When the offering period is 6 months companies use the purchase period and offering period interchangeable. But if the offering period is long (for example 1 year) then there will be multiple Purchase periods. For example The offering period is 12 months. The purchase period is 6 months. Then stocks would be purchased twice at the end of the purchase price.

Grant Date The grant date is usually the first day of the offering period. This is sometimes called the enrollment date. In ESPP grant date is important for tax purposes and for lookback price it also serves as a point for calculating the stock price.

Purchase Date or Exercise Date: Pre-determined date upon which stock is bought for all employees who have opted for ESPP. If there are several purchase periods during a single long offering period, there will also be several purchase dates (one at the end of each purchase period). For example, a 12-month offering period that includes two purchase periods will have a purchase date at the end of every six months.

Purchase (or Exercise) Price: The purchase price of a share of stock bought at the end of a purchase period or offering period. If the ESPP includes a lookback provision the purchase price will be determined by comparing the market price of a share of stock on the offering date with the market price of a share of stock on the purchase date and applying a discount to the lower of the two prices. Check whether your plan allows the purchase of fractional shares or only whole shares with your payroll deductions. If only whole shares, any amount remaining in your account may be rolled over to the next purchase period (without interest).

Lookback: If your ESPP has lookback provision then your purchase price is based on the stock price at either the first day or the last day of the purchase period, whichever is lower. For example If the price at the start of the period is Rs. 100 and at the end is Rs. 70, then the lower one or Rs. 70, is the price at which stock will be purchased. If a company allows a discount then it is applied to this price.

Discount: Discount given by the company to the purchase price. Company policy determines How much discount can one get. Discount is typically up to 15% for US based company.

Example of Lookback and Discount: Stock price of your company during the six-month offering period was $10 at the start and $12 at end of the period and you get 15% discount and have lookback provision. So $10 is the purchase price as it is the minimum price during the purchase period. As you get a 15% discount so you get stocks at $8.50 ($10 – 15% of $10).

If the stock price at the start was $12 and at the end was $10 then purchase price would still be $10 and you would have got stuck at $8.50 ($10 – 15% of $10)

Qualified: means there is no tax until you sell your shares. nonqualified your employer will withhold taxes at the time of purchase. (An advantage of a nonqualified plan is that it allows the employer to offer a discount greater than 15%.)

Tax and ESPP

Where there is money there are taxes and brokerage. For foreign listed stock exchange one needs to also consider currency conversion rate(difference in Rs – $) between the purchase date and sell date.

Perquisite: As the company is giving you a discount on the stock price this part of salary comes under perquisite and hence is taxed as per your tax slab. So if you are in 30% tax slab as , ESPP contribution will be taxed at 30.9%(include education cess etc).

Perquisite is calculated on the difference between the Market price and the allotment price at the time of purchase. So if you got 10 shares when the market price of the stock was $12 and you got at $8.5 then you would be taxed on 10* ($12-$8.5) = $35= Rs 35 * US Dollar conversion rate one the date of allotment. On this company will deduct tax as per your income slab. Hence your actual discount becomes ~10%. This would be deducted by your company as TDS and deposited to the Indian Government. It would also be reflected on your Form 12BA. Our article Understanding Form 12BA explains perquisite and salary in detail.

Brokerage: When you sell the shares the brokerage company also charges for sale of shares and for wiring funds to India. At times they also deduct TDS (called as Withholding tax in the US) from the sale proceeds.

Tax: The income earned from the sale of shares and tax on it depends on whether the shares are listed on Indian stock exchange or not and the time period for which you hold the shares. It is calculated as following:

For stocks listed on Indian stock exchange

Income earned from stock comes under the category of Capital Gains. For stocks the capital gain is difference in the selling price and buying price.

- If you sell the shares within 1 year of getting the shares, then the gains are called Short Term Capital Gains (STCG) and you pay 15% tax on the profit earned.

- If you sell the shares after 1 year of buying shares, then the gains are Long Term Capital Gains (LTCG). There is no tax on long term capital gains.

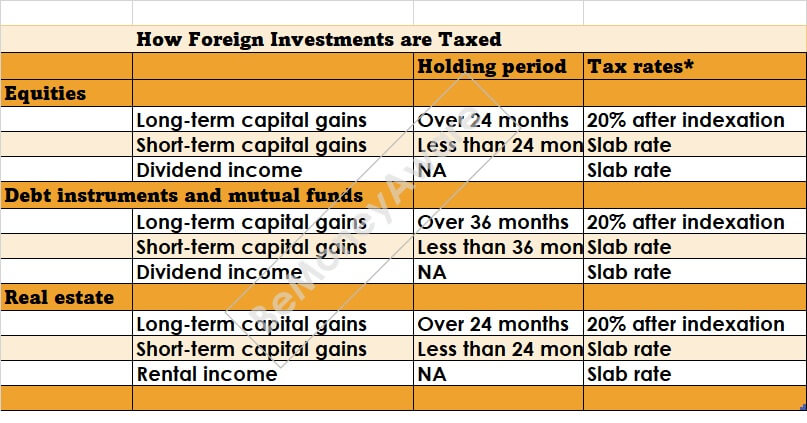

For stock listed on the foreign stock exchange

- If you sell the shares within 2 years(24 months) of getting the shares, then the income(the difference between selling and buying price) is taxed as per your income tax slab.

- If you sell the shares after 2 years of buying shares, then the gains are taxed as Long Term Capital Gains (LTCG). You have to pay 20% with indexation on profit. You will have to fill these details in ITR2 in capital gain section CG-OS. Our article Cost Inflation Index, Indexation and Long Term Capital Gains has information on indexation, calculation of Long term capital gain in detail.

Example of STCG: you got 100 shares of your company which is listed in the US on 18 Jul 2014 at $8.50 when USD is 59.93 INR. Say you sell the share on 17 Jan 2015 when USD is 61.63 If you sell at any time before 19 Jan 2016) at $12, then the difference is added to Income. 10= * (61.63 – 59.93) * (12-8.5) = Rs 595

Example of LTCG, you got 10 shares of your company which is listed in the US in Nov 2011 when the market price was $20 and indexation was 711 and 1USD=51.99 Rs and you sold shares sold for $40 in May 2013 when 1 USD= 56.3855 and indexation was 939. A commission of $20 was charged by the brokerage.

- Sale Price of 10 shares = 10 * $40 = $400 = Rs. 400 * 56.3855 = Rs. 22,554.2

- Purchase price of 10 shares = 10 * 20 = $200

- Indexed cost of acquisition = $223.5 * 939/711 = $ 264.14 = Rs. 264.14 * 51.99 = Rs. 13,732.38

- Expenditure on transfer = $20 * 10/100 = $2 = Rs. 2 * 56.3855 = Rs. 112.771

- Long term capital gain = Rs. 22,554.2 – Rs. ( 13,732.38 + 112.771) = Rs. 8709.049

- Tax on Long term capital gain is 20% of 8709.049 = Rs 1741.8098

How foreign Investments are taxed for Indians

Alternatives to ESPP: RSU and ESOP?

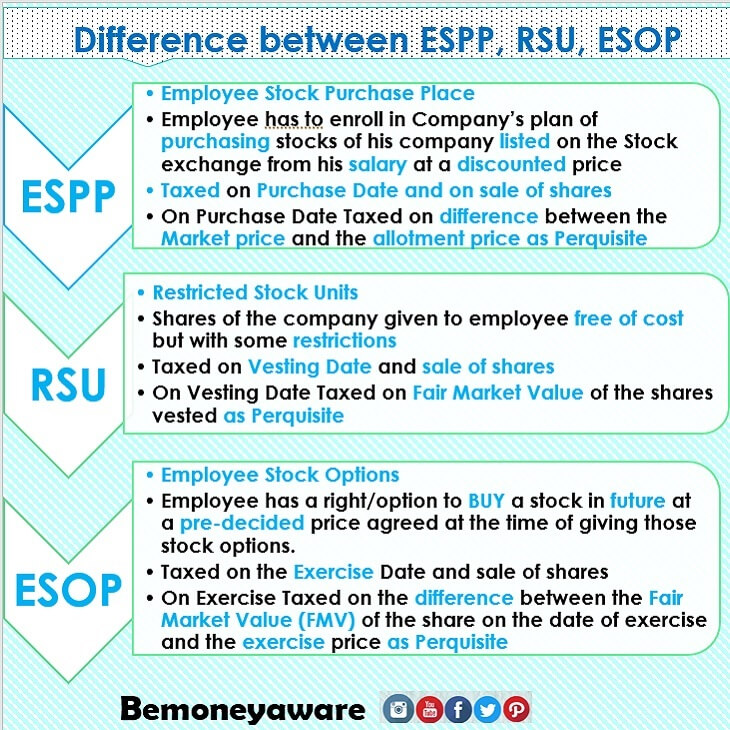

Restricted Stock Units(RSU) represent an unsecured promise, i.e no strings attached, by the employer to grant an employee a set number of shares (at zero strike price) on completion of the vesting schedule or other conditions. Basically, your purchase price is 0. Our article RSU of MNC, perquisite, tax , Capital gains, ITR, eTrade explains it in detail.

Employee Stock Options Program (ESOP): The employee has the option to purchase the stock of the company at a future date at a pre-determined price. An employee can buy or not exercise his option on the date. Our article What are Employee Stock Options (ESOP) explains it in detail.

What is difference between ESPP, RSU and ESOP?

Related Articles :

- RSU of MNC, perquisite, tax , Capital gains, ITR, eTrade

- Salary, Net Salary, Gross Salary, Cost to Company: What is the difference

- Variable Pay

- It’s not what you earn that makes your financial position!

- Understanding Form 16: Part I

- Basics of Employee Provident Fund: EPF, EPS, EDLIS

- How to Calculate Income Tax

Hope this article helped you in understanding what is ESPP? How different it is from ESOPs and RSUs? Have you availed of ESPP? Would you suggest going for ESPP?

Hi,

I wanted to know what would be the initial value of investment in A3 incase of ESPP where stocks are bought on discount and difference between FMV and purchase price is added to Perquisite in salary and TDS is deducted.

Also what would be the initial investment incase of RSUs.

Adding to this what is peak value of investment during the Period. Is it calculated from everyday closing value of the share or the peak it achieved during trading sessions.

Adding these points would be superb to your wonderful article. Thanks a lot.

For listed LTCG is there no tax or is there 10% tax in excess of 1 L profit? Can you confirm please?

For listed LTCG is there no tax or is there 10% tax in excess of 1 L profit?

only for the stocks listed on Indian Stock exchanges

For international tax different rules apply!

I have stocks acquired through ESPP from a US MNC. I am leaving the firm and want to keep these stocks. Can I transfer these stocks to my India DMAT account? This MNC is not listed in India.

Sadly no.

You cannot transfer your US MNC stocks to Indian Demat Account.

Hi,

I have invested in ESPP in my company. But I am not sure how to declare that in FA for in ITR2. The scenario is as such:

1. I purchased 20 stocks in a period of 1 year at price of $40 each(Grant price).

2. The purchase price was $90.

3. The taxation which my organization is calculating, is on the difference in grant and purchase price like ($90-$40)*20 = $100

4. With conversion rate of INR 70 my taxable amount becomes = 100 * 70 = 7000

5. Now what amount must be declared in following fields in the FA form:

Total Investment, Income Derived from asset, Income taxable amount,

Schedule where offered, Item number of schedule

Request you to please help me in this.

P.S. – I have not sold even a single share till this time.

Total investment is $1800

Hi,

I have invested in ESPP in my company. But I am not sure how to declare that in FA for in ITR2. The scenario is as such:

1. I purchased 20 stocks in a period of 1 year at price of $40 each(Grant price).

2. The purchase price was $90.

3. The taxation which my organization is calculating, is on the difference in grant and purchase price like ($90-$40)*20 = $100

4. With conversion rate of INR 70 my taxable amount becomes = 100 * 70 = 7000

5. Now what amount must be declared in following fields in the FA form:

Total Investment, Income Derived from asset, Income taxable amount,

Schedule where offered, Item number of schedule

P.S. – I have not sold even a single share till this time.

Hi,

What happens if i sell the shares in losses?

You show it as a capital loss.

You have a chance to offset it in the next 8 years if you file ITR in time.

Income comes under five heads – salary, income from house property, income from business and profession, capital gain and income from other sources. The law allows you to set off losses in one against gains in another, depending upon the various criteria.

However, tax laws allow setting off of losses against gains in the same category, based on different criteria. If an income is tax-exempt, it however cannot be adjusted against any loss from an income that is taxable. For tax computation, profit or losses in shares are clubbed under the head of capital gains.

If an investor has held shares for less than 12 months from the date of buying, then the resulting loss on its transaction on stock exchanges, if any, is termed as short-term capital loss (STCL).

This loss can be adjusted against the short-term capital gain (STCG) or long-term capital gain (LTCG) from shares, if any, thus lowering the tax outgo. Short-term capital gains from equities are taxed at 15 per cent. (If an investor has held shares for more than 12 months, then the resulting gain/loss is termed long-term capital gain/loss.)

If the short-term loss cannot be set off in the same fiscal, then the balance can be carried forward to subsequent eight years. In each of these, the said short-term losses can be set-off against short-term capital gain (STCG) or long-term capital gain, if any.

To reduce outgo, many investors set off gains made from equities in the fiscal against losses occurred in same year or previous year. They book losses, if any, on existing holdings and then later repurchase the stock to keep their holdings intact.

For example, an investor has already booked short-term profit (by selling within 12 months) of Rs. 10,000 in some stocks. At the same time, the investor is sitting on un-realized loss of Rs. 4,000 in some other stocks.

In that case, the investor has to pay short-term capital gains tax at 15 per cent on Rs. 10,000 profit. To reduce short-term capital gains tax liability, the investor can sell the stock on which he is incurring Rs. 4,000 of losses. In that case, the investor’s has to pay tax on Rs. 6,000 (Rs. 10,000 – Rs. 4,000), not Rs. 10,000. To keep his holding intact, the investor can later repurchase the stock.

However, long-term capital losses on shares can only be set off against long-term capital gains, if any. Further, any long-term capital losses that cannot be set off against long-term capital gains arising in the same fiscal can be carried forward to subsequent eight years.

Awesome article. Thanks for publishing it. It will be great if you can publish with revised tax rules introduced in 2018 budget.

Hi,

I bought all my vested stocks on April 8 2015 and my company listed on Nasdaq on April 24, 2015. I sold my all shares on Nov 2016. Is it long term or short term in Indian taxation system.

Very nice article… Thanks for sharing…

For LTCG on foreign stocks, is it not true that minimum holding period of the stocks should be 3 years?

In “Example of LTCG”, how is the value $223.5 derived for calculating “Indexed cost of acquisition”?

that seems a typo, 264.14*711/939 gives 200, so 223.5 should have been a 200. Either a typo, or on purpose to confuse readers.

It is 223.5 * 939/711 not the other way round

Hello,

I file my returns online. I could not find a section under ITR where I could fill in the details of the ESPP and RSus granted to me. Please help me understand where these details should be filled in case an individual files the returns online.

Which value should be considered as purchase price for calculating STCG. Should it be actual purchase value post company discount(e.g. $8.5) or should it be FMV on date of purchase/allotment (e.g. this could be either $12 or $10 based on situation) or should it be base value on which discount is offered (e.g. $10 in this case) ?

Would this be a beneficial option if one opts for QuickSale,where in most cases it’s sold for around same price as that on date of purchase.

Hi Anil,

Can you please let me know what is the process of TAX deduction on ESPP in india?

Lovely article. Hope it is up to date with the current taxation policies and norms.

Thanks for your kind words. They are very encouraging to us.

Did you find anything missing?

Hi Kirti,

Section 2(42) of IT Act says duration as 36 months to be qualified LTCG for stocks not listed in india. Has anything changed in between? can you please clarify the source of info.

https://indiankanoon.org/doc/1595434/

that’s correct. foreign stocks are considered unlisted securities.

Thanks for the wonderful article, very informative, Can you please help me understand in the example of “Example of LTCG” for the calculation of “Indexed cost of acquisition” how is value of “$223.5” is arrived? Also in calculation of “Expenditure on transfer” is it constant as 10% of the 1 share at buy price?

Thanks a lot. It clarifies many things. I have been calculating my gains differently for my NYSE listed RSU and ESPP. I was calculating the gain/loss in USD and applying the currency conversion rate on the day of sale for changing it to INR. Can you give which section in the IT act gives the information of foreign capital gains, if possible?

1. My broker maintains the ESPP and RSU stocks related statements separately. So some times I sell the shares allotted later before the earlier alloted shares. Should I still follow First in First out for the computation. Broker maintains each grant related purchase and sale separately in the statement.

2. Can I add currency conversion losses to the sale proceeding calculation?

Thanks a lot again.

I have the following two questions regarding LTCG computation in the above article …

1.Is it right only 10% of brokerage can be claimed as expenditure on transfer ?

2.For RSU LTCG, is it right one will still go by the FMV on the date of grant as its purchase price, assuming perquisite tax was paid for it ?

For STCG, shouldn’t it be (selling price) – (purchase price).

purchase price = $8.5 * 100 = Rs 59.93 * 8.5 * 100 = Rs 50,940.5

selling price = $12 * 100 = Rs 61.63 * 12 * 100 = Rs 73,956

STCG = RS 73,956 – 50,940 = 23,016

Thanks for input Rahul. We appreciate it.

We looked at it and corrected it.

Please note that purchase price is 12 $ and not 8.5$ the price at which you got shares. This is because the difference between the price you got and Fair Market Value, was perquisite for you and your company paid tax on it. Tax on the shares should be mentioned in your Form 12BA and Perquisite in Form 16.

Very informative website. keep up the good work.

Thanks for the encouraging words.

Very informative website. keep up the good work.

Thanks for the encouraging words.