Insurance is a contract and it is important for the policyholder and also his or her nominees to understand the rights and the process of claim so that person or the family is not denied the benefit at a time it needs the most. This article explains how to claim life insurance on death of insured.

How to claim Life Insurance Policy

What is a claim?

A claim is a formal request to an insurance company asking for a payment based on the terms of the insurance policy. Insurance claims are reviewed by the company for their validity and then paid out to the insured or requesting party (on behalf of the insured) once approved. Claim settlement is one of the most important services that an insurance company can provide to its customers. In this article we shall focus on claim of Life insurance policies.

Types of claims

A Life Insurance Policy results into claim in the following situations:

- On maturity of the policy for example in cases of endowment policies or moneyback policies on completion of the term for which the insurance was taken even when policy was made paid up.

- On death of the life insured, if it occurs before the maturity of the policy, provided the policy is in force on the date of death

Who is entitled to receive the claim benefit?

- Life Assured himself in case of policy on own life for living benefit claims i.e. claims under endowment plans etc

- The nominee or the appointee (in case of minor nominee) last recorded under the policy in case of policy on own life.

- The proposer in case the policy is not on own life.

- Assignee in case the policy is assigned.

Maturity Claims

- In case of Endowment type of Policies, amount is payable at the end of the policy period. The Insurance company which services the policy sends out a letter informing the date on which the policy money is payable to the policyholder ( at least two months in case of LIC) before the due date of payment. The policyholder is requested to return the Discharge Form duly completed along with the Policy Document. On receipt of these two documents post dated cheque is sent by post so as to reach the policyholder before the due date.

- Some Plans like Money Back Policies provide for periodical payments to the policyholders provided premium due under the policies are paid. In the cases where amount payable is less than a fixed amount (up to Rs.60,000 in case of LIC), cheques are released without calling for the Discharge Receipt or Policy Document. However, in case of higher amounts these two requirements are insisted upon.

Death Claims

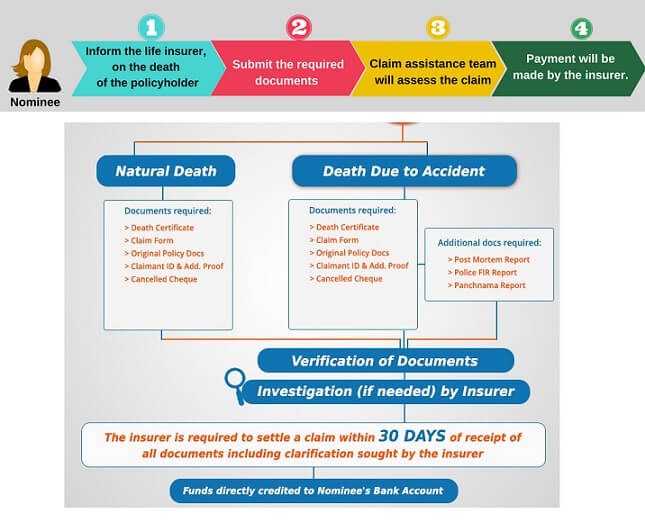

The death claim amount is payable in case of policies where premiums are paid up-to-date or where the death occurs within the days of grace. Process to claim insurance is as follows:

Intimation : The nominee or assignee of the policy, who is entitled to receive the benefits, needs to inform the insurance company about the loss. The intimation of death should be in writing and accompanied by a copy of death certificate. It should contain details such as date, place and cause of death,policy number,claimant’s relationship with the assured or his status (nominee, assignee, etc.). This needs to be submitted at the nearest branch office of the insurance company.

Claim form: On receipt of the intimation of demise, the branch office provides the relevant claim form to the applicant. This claim form needs to be filled and submitted to the insurance company along with the necessary documents. For example in case of LIC one needs to provide a) Claim form A – Claimant’s Statement giving details of the deceased and the claimant. b) Certified extract from Death Register c) Documentary proof of age, if age is not admitted d) Evidence of title to the deceased’s estate if the policy is not nominated, assigned or issued under M.W.P. Act. e) Original Policy Document. Additional forms are called for if death occurs within three years from the date of risk or from date of revival/reinstatement explained on LIC website Death Claims.

Documents : The insurance company may require the death certificate, policy document, deeds of assignments/ re- assignments, if any, legal evidence of title, if the policy is not assigned or nominated, medical attendant’s certificate and other documents as applicable.

Processing: The insurance company may appoint an investigator to ascertain the validity of the claim. If it is found to be valid, the amount is paid, otherwise a repudiation letter is sent to the claimant, listing the reason for rejection. An insurer, upon receiving a claim, should process it without delay. Any query about additional documents shall be raised at once and not in a piece-meal manner, within a period of 15 days of the receipt of the claim. A claim under a life insurance policy should be paid or be disputed giving all the relevant reasons within 30 days from the date of receipt of all relevant papers and clarifications required. However, if in the opinion of the insurance company the circumstances of a claim warrant an investigation, it shall initiate and complete it at the earliest, not later than six months from the time of lodging the claim.

The process is shown in the picture below

Points to note

- Please keep the list of The life insurance policy documents should not be kept in safe deposit lockers as these are usually sealed temporarily on the owner’s death and may delay the settlement of claim.

- An agent’s key responsibility is to assist the policyholder in getting the claim. Since he is the one who had initiated the policy documents, he would be the best person to get the claim out most effectively and efficiently. Thus, the agent needs to be contacted who had taken the policy for the life insured. In case, the agent is not known or not contactable, then the Insurer’s office needs to be contacted.

- In case there is no nomination or assignment in a policy, the benefit will be paid out only after the claimant has provided documentary proof of entitlement.

- All life insurance policies have a two-year contestability, which means during that period, a large number of claims get rejected because of investigations by the insurance company. This is not to suggest that claims made after two years are never rejected. If the contract is based on any fraudulent statement by the policyholder, the claim could be rejected, no matter when the policy was bought.

- The amount that one gets from life insurance policy is tax free.

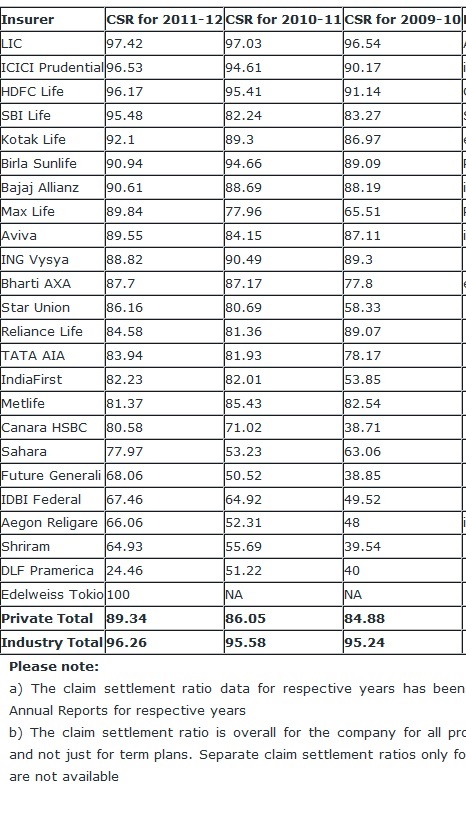

Claim Settlement Ratio

Claim Settlement Ratio (CSR),is the number of claims settled by the insurance company out of every 100 claims it has received. It gives us an idea about the claim solving ability of the insurance company. The IRDA has made it mandatory for all insurance providers to publish claims related data in the public domain. More detail at IRDA.gov.in Tip for buying life insurance look at companies with claim acceptance ratio more than 90%.

Claim Settlement Ratio

Related Articles

- Checklist for buying Life Insurance Policy

- Paper Work A Necessary Headache

- Insurance at every lifestage

- Discontinue Life Insurance Policy: Surrender,Paid Up,Loan

- Basics of Insurance

The Claim process seems simple but it is usually not hassled free. We must remember since an insurance contract is based on the principle of utmost good faith, it is important that the customer is honest in his declarations and abides by the policy agreement. Did you need to claim the insurance? How was the process?