The new ITR forms for FY 2022-23 or AY 2023-24 are broadly similar to that of the previous year with some additional details required such as Virtual Digital Assets (VDA) asset or minor tweaks for new regime. This article explains What are the changes in the ITR Forms for AY 2023-24?

The new ITR forms will come into effect from April 1, 2023. The Changes in ITR forms are as follows:

- There are no changes in ITR-1.

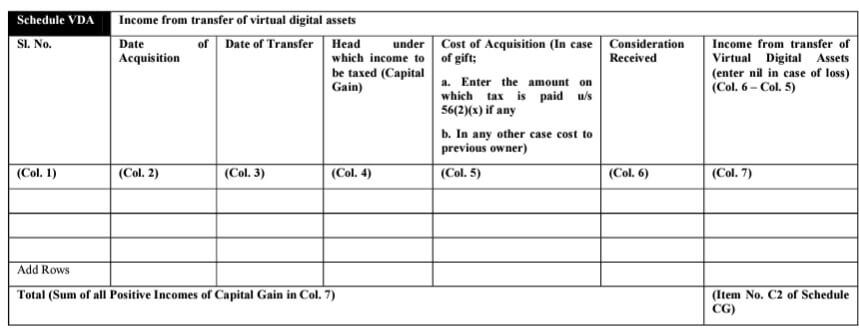

- Virtual Digital Assets: you will now need to report Virtual Digital Assets (VDA) details. In all forms other than ITR1, a new schedule for reporting Income from Virtual Digital Assets has been included under the head Capital Gains. One need to report the date of acquisition, date of transfer as well as the cost of acquisition and the proceeds received on the sale of VDAs. Income from VDA must be reported quarterly,

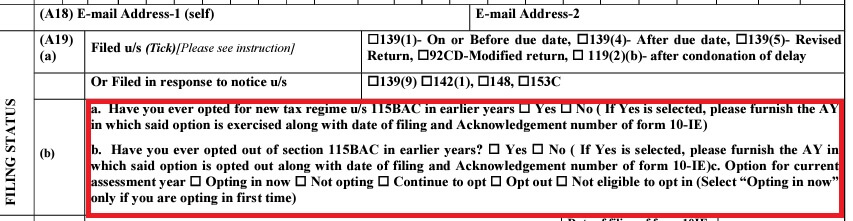

- New Tax Regime: A new questionnaire in ITR 3 and ITR 4 has been added to determine if the taxpayer has opted out of the New Tax Regime in previous years.

- The income from trading has to be bifurcated into intra-day trading and delivery-based trading also and reported accordingly in ITR3/ITR5/ITR6

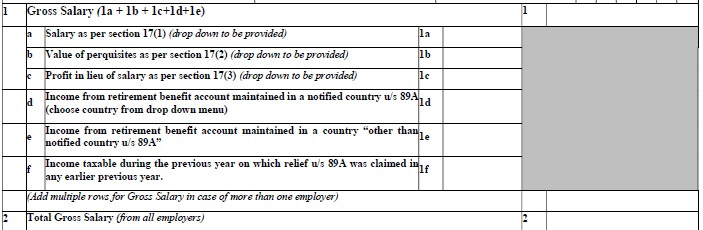

- Salary and Income from other sources: A new disclosure has been added for ‘Income from retirement benefit accounts’. Disclosure is required to be made about the taxable income on which relief under section 89A was claimed in any of the earlier years.

- Common ITR form: While the CBDT had released common ITR form for public consultation in November 2022, the new forms notified are separate ITR forms and one would need to wait for common ITR. Our article covers New draft Common Income Tax Return Form

- The last for filing the income tax return for the assessment year 2023-24 or financial year 2022-23 is July 31, 2023

Table of Contents

Virtual Digital Assets, Tax and ITR

From 1 April 2022, a new Section 115BBH was introduced for tax on cryptocurrency and other VDA (Virtual Digital Assets) and a new Section 194S for the deduction of TDS on the transfer of virtual digital assets.

As per Section 2(47)(A) of the Income Tax Act, a Virtual Digital Asset (VDA) includes cryptocurrency, Non-Fungible Tokens (NFTs), and any other digital asset notified by the central government in the official gazette.

- Person responsible for making the payment on the transfer of cryptocurrency must deduct TDS at a rate of 1% under Section 194S if the aggregate transfer amount during the financial year exceeds INR 10,000. The said limit is INR 50,000 in the case of specified persons.

- Income from the transfer of cryptocurrency, NFT, and other virtual digital assets is taxed at a flat rate of 30%.

- Capital Gains = Full Value of Consideration (Selling Price) – Cost of Acquisition (Purchase Price)

- Deductions on transfer of VDA

- The taxpayer cannot claim any expense or allowance against such income.

- The taxpayer can claim the cost of acquisition i.e. purchase price as a deduction from the income.

Thus, Taxable Income = Selling Price – Purchase Price.

- Loss from transfer of cryptocurrency cannot be set off loss against any other income. It cannot be carried forward to future years.

- Loss under any other head of income cannot be set off against profit on transfer of cryptocurrency

- A gift of cryptocurrency, NFT, or other VDA is taxable in the hands of the receiver.

If you made any income from crypto and other virtual digital assets in FY 2022-23 then you will have to report such income in a separate schedule provided in the new ITR forms. The details that you need to provide include finer points like the date of acquisition, date of transfer and head under which income to be taxed (capital gain). If you received crypto/VDA as a gift, then you will have to provide the details of the amount on which tax has been paid for the transfer of the asset.

Reporting of tax on Cryptocurrency, VDA in ITR Form

New Tax Regime

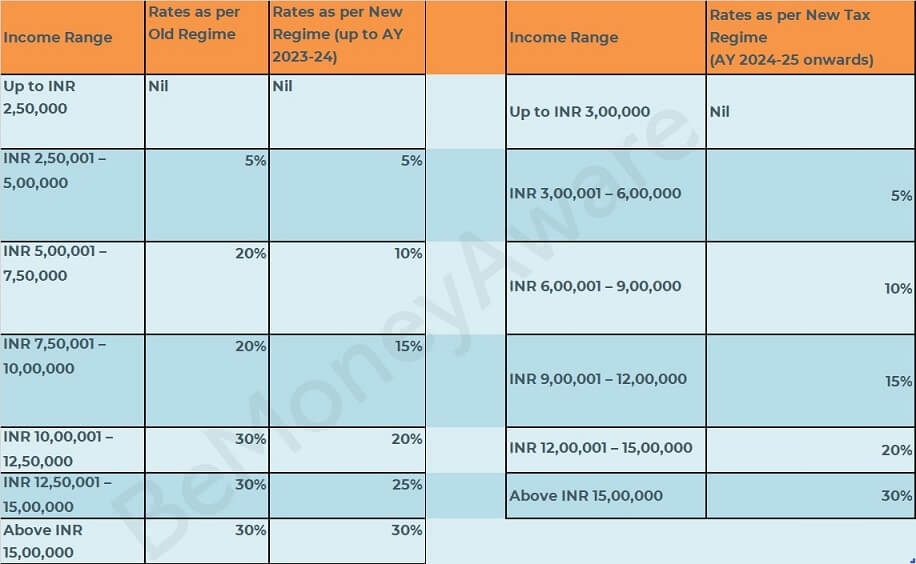

The new tax regime was introduced from 1 Apr 2020 to simplify taxes and reduce the burden of compliance on taxpayers. The major difference between both old and new tax regimes is income tax slab rates and the ability to claim exemptions and deductions. in Union Budget 2023-24 the tax slabs were revised for the new regime along with other changes.

Now taxpayer has a choice to Take Deductions and stick with the old tax slabs and not take deductions and opt for new tax slabs. Which one should one choose? People availing deductions like interest on home loans, health insurance, and PPF would need to evaluate as in their case, the old regime could still prove more tax efficient.

Details in our article Old or New Tax Regime?

New or Old Tax regime in ITR3/ITR4

New or Old Tax regime in ITR1/ITR2

To choose old or new Tax System

- Calculate all the deductions you will take

- Find tax using the old system.

- Find tax using the new system

- Find the difference

- Check the paperwork required to claim, if it is worth it. For example if you want to take Insurance policy to save, understand the payment frequency, returns etc.

Tax slabs rates in old and new tax regime

Traiding, Income Tax and ITR

A Trader buys and sells stocks and securities with an intention to earn quick profits due to fluctuations in prices. Trading Income comprises equity (delivery, intraday, F&O), commodity trading, currency trading, etc.

From FY 2023-24, The income from trading has to be bifurcated into intra-day trading and delivery-based trading also and reported accordingly in ITR3/ITR5/ITR6

Our article Income Tax on Selling Shares: Trading, Capital Gains, ITR covers it in detail

- How to Show Capital Gain on Shares and Equity Mutual Funds in ITR

- Presumptive Taxation Scheme for Professionals, Small Business, sections 44ADA, AD,AE

- Stocks: Trading stocks may be treated as either capital gains or business income.

- Intraday Trading means buying and selling stock on the same day. Income from equity intraday trading is a speculative business income and tax has to be filed under the head PGBP (Profits & Gains from Business and Profession).

- The income from F&O trading is a non-speculative business income. Non-Speculative Business Income is taxable at slab rates.

- When the trader has done significant share trading activity with regular trading in shares and securities or in futures and options during the year, the income from such activity is classified as Business Income.

- When the volume of trading transactions is less and it is not a regular activity, the income from such activity is classified as Capital Gains

- All other forms of trading are considered to be Business Income as per Income Tax.

- The applicability of the Tax Audit is determined on the basis of Trading Turnover and the Profit or Loss on it. In the case of a stock trader, a Tax Audit is applicable in the following situations:

- If trading turnover is up to INR 2 Cr, the taxpayer has incurred a loss or profit is less than 6% of Trading Turnover and total income is more than the basic exemption limit.

- If trading turnover is more than INR 2 Cr and up to INR 10 Cr and the taxpayer has incurred a loss or the profit is less than 6% of Trading Turnover.

- When trading turnover is more than INR 2 Cr and up to INR 10 Cr, profit is more than or equal to 6% of Trading Turnover, and the taxpayer does not opt for the Presumptive Taxation Scheme under Sec 44AD

- Trading Turnover is more than INR 10 Cr.

- When the trading income is treated as business income, it is important to calculate the trading turnover to determine the applicability of the Tax Audit as per the Income Tax Act.

Type of Trading Calculation of Trading Turnover Equity Intraday Trading Absolute Profit Futures & Options Trading (Equity, Commodity, Currency) Absolute Profit Equity Delivery Trading & Mutual Fund Trading Sales Value

Advance Tax

If the tax liability of the trader or investor is expected to exceed Rs. 10,000, then they must calculate and pay Advance Tax. This is so as to avoid Interest under Section 234B and Section 234C.

Advance Tax is to be paid in quarterly installments on 15th June, 15th September, 15th December, and 15th March.

However, if trader opts for presumptive taxation u/s 44AD, they must pay the entire amount of Advance Tax in a single installment on or before 15th March.

Filing of ITR

- If a trader has Income from Capital Gains, then he/she should file ITR-2.

- If a trader has Business Income, then he/she should file ITR-3.

- The trader who has opted for the Presumptive Taxation Scheme should file ITR-4 on the Income Tax Website.

Income from Retirement Benefits section 87A

If one worked in a country outside of India for many years and contributed to the retirement benefits in that country and then came back to India, how would his retirement benefits be taxed? For example Rajan worked in USA for 10 years and came back to India . He contributed to Retirement benefit account in USA while he was Non-Resident to India and as per Indian Income Tax laws he is resident of India.

The Finance Act, 2021, inserted a new Section 89A in the Income-tax Act, 1961, (ITA), to provide relief to residents who have income from foreign retirement benefits accounts.

According to Section 89A,

- the income from the accounts opened in a foreign nation will not be taxable on an accrual basis. The foreign country will subject his income to taxation at the time of withdrawal.

- The amendment is effective from April 1, 2022, which will apply to the assessment year (AY) 2022-23 and subsequent AYs.

- The US, the UK, Canada, and Northern Ireland are the notified countries for Section 89A , as per the Central Board of Direct Taxes (CBDT).

- The CBDT has also notified Rule 21AAA and Form 10-EE to claim the relief under Section 89A regarding the income from foreign retirement funds.

- A new disclosure has been added for ‘Income from retirement benefit accounts’. Disclosure is required to be made about the taxable income on which relief under section 89A was claimed in any of the earlier years.

Income from Retirement Benefits in ITR

Types of ITR

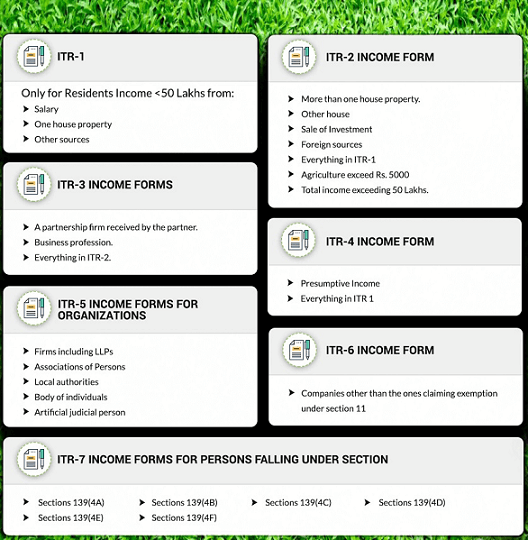

At present, depending upon the type of person and nature of income, taxpayers are required to furnish their Income-tax Returns in ITR-1 to ITR-7.

Govt has proposed a common ITR by merging all the existing returns of income except ITR-7. However, the current ITR-1 and ITR-4 will continue. This will give an option to such taxpayers to file the return either in the existing form (ITR-1 or ITR-4), or the proposed common ITR, at their convenience.

Different Types of ITR forms

Related Articles:

- Old or New Tax Regime?

- Advance Tax

- How to file ITR Income Tax Return, Process, Income Tax Notices

- Income Tax on Selling Shares: Trading, Capital Gains, ITR

- How to Show Capital Gain on Shares and Equity Mutual Funds in ITR

- Presumptive Taxation Scheme for Professionals, Small Business, sections 44ADA, AD,AE