Goal setting involves deciding the end point of your planning exercise, determining where you want to go. The more tangible the goals your goals, the easier it is to plan their realisation. Begin by listing down both your short and long term financial goals. That’s how the book, You Can Be Rich With Goal based Investing, by PV Subramanyam and M Pattabiraman begins. This article is a review of the book .

Table of Contents

Overview of the Book You Can Be Rich With Goal based Investing

The book is an attempt at making investing very common sensical and simple. It is meant for beginners and young earners to quickly understand the basics and implement them. The book also caters to experts who will find the sections on mutual fund selection, portfolio construction, and the online calculators useful.

- Book is written by PV Subramanyam of financial blog subramoney, and M. Pattabiraman of (freefincal.com). Subramoney.com is a financial blog that raises the questions and also answers them. His first book, Retire Rich – Invest Rs. 40 a day, has sold more than 150,000 copies so far. M. Pattabiraman (pattu) is an associate professor at the IIT Madras. He publishes ‘how-to’ articles , research and posts open-source calculators on personal finance, mutual funds and stocks on his blog. These Two personal finance bloggers, have around 8 million site views between them,!

- This book is a crisp non-technical description of money management and does not contain a single equation!

- There are about 9 calculators associated with the book. They are hosted online and those who have register at goalbasedinvesting.in can access them

- There are 11 chapters in the book. Most of the are less than 10 pages long and each chapter ends with a worksheet. The chapter which runs into 20 pages is Chapter 10 Mistakes to be avoided.

- The topics covered in the book are given below.

- 1 Where are you today?

- 2 Where do you want to go?

- 3 What resources do you have?

- 4 How much risk can and will you bear?

- 5 Allocating your assets to minimise risk

- 6 A vehicle called mutual funds

- 7 Portfolio construction requires discipline not IQ.

- 8 Life and Health Insurance

- 9 Records to be maintained

- 10 Mistakes to be avoided

- 11 How to stay away from new products

- Appendix 1 : More about Mutual Funds. a detailed description of equity and debt mutual funds and how to choose them.

- Appendix 2 : Description of Calculators

- Appendix 3: Glossary

.The YouTube video gives an overview of the book

Inside the book Goal based Investing

Lets go through the various chapters in the book, Goal-based Investing or the book which shows how to Take Charge of your Finances.

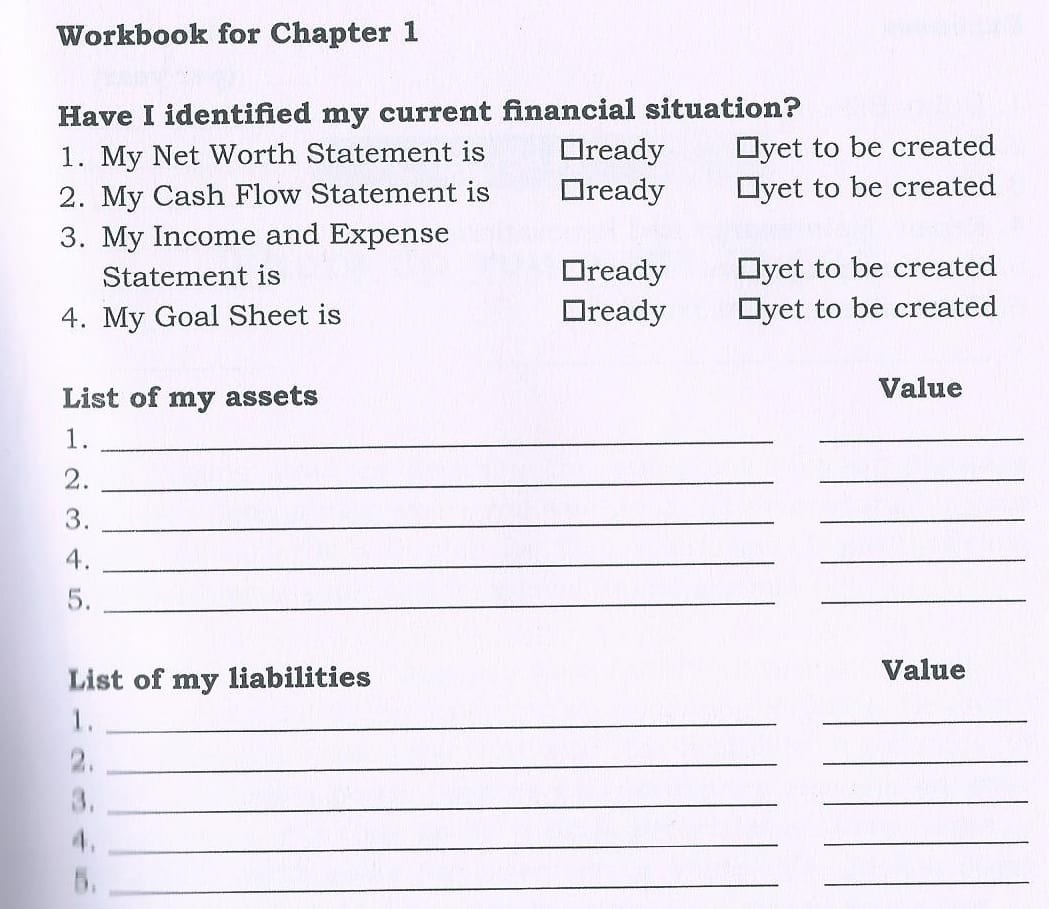

Where are you today? : Chapter 1

First step of Goal Based Investing is to come up with 4 documents that that allow you to take charge of your financial life

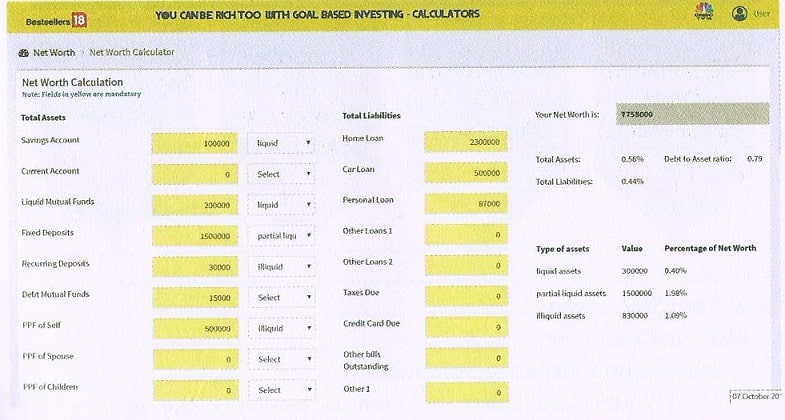

- Your Net Worth : Difference between your Assets and Liabilities(Assets- Liabilities). Assets are things that you own and for which there is a reasonable market value ex Bank Balances, shares of your demat account, Your EPF etc. Liabilities are your unpaid credit card, loans.

- Income and Expense statement : How much you are earning and how much are you spending

- Your Cash Flow : How much cash you received during a particular month or year and how you used it

- And your Goal sheet: Statement of where you want to go.

Ex of Worksheet of Chapter 1

Ex of Net Worth Calculator

Goals :Chapter 2

Short term Goals are things you want to achieve within next 5 years : a car, wedding. If your short term goals require extraordinary returns its time to do a little prioritising. Drop some of the goals ; push them for later, make a trade off, pick a Nano instead of Honda city.

Long term Goals stretch over a period of 10-30 years. These could include education fund for children, buying or selling a business, a special vacation or a second home.

Many people do not have their OWN financial goals, so that they do a cut-n-paste job. Means they take society goals and cut paste them into their own life. For example Goals that a Society wants to have for a boy are (Goals for Girls are different)

- At 22 he should have a nice Engineering degree from IIT

- He should join IIM(A)

- At 27 he should get married to a nice girl from the same community

- At 30 have a kid, at 33 repeat the performance.

- He should have a nice big car, a large house (size depends on location but a 3 BHK is a must; if it is a 7 BHK well you are successful)

But the Boy goals, after getting a IIM A degree as per the parents wishes, can be See various parts of Africa and South America by the time I am 30. Work for a few years in the USA and see the whole of US by age 33. If I meet a like minded girl I’ll marry her and assume that she will earn and spend along with me, If we have a kid great, or we will continue with mountaineering and cycling tours till we reach 40 years of age.

How much is risk can and will you bear? : Chapter 4

What would you do if you see lion in the forest?

- Run!

- Freeze!

- Ignore it is a male Lion and someone in Quora said males do not hunt.

During a mock quiz we are likely to answers (a) Run. However in real life many of those who answered(a) may actually resort to Freeze. As Human beings tend to be more logical during a mock quiz (when the score does not matter) than in real life. Risk profiling refer to the process by which an investor/advisor tries to answer following questions

- What is risk and how does it differ from volatility.

- What is the volatility that we should stomach for each of our financial goals.

- What is the volatility that we can stomach for each of our financial goals? Answer to this lies in “What kind of a person am I?” Am i one to handle stressful situations on my own or am I one who needs help?

- How should we reconcile the two?

So what would you do if the stock market fell by 40% over the course of a few weeks?

- a) Do nothing

- b) Buy more

- c) Sell

Allocating your Assets to minimize risks : Chapter 5

Asset allocation is one of the more over used and misused concept. Asset allocation is putting your money in 3-4-5 asset classes,depending on your knowledge and market access Asset allocation is not a wealth creation tool. At best it is a wealth protection tool. Somewhat like insurance , it cannot make you rich but ensure that you do not become poor because of an accident. It suggests Asset allocation during different life stages in life. Whatever asset allocation you chose, if it keeps you awake at 3 a.m, it is not a good equation that you have got.

A vehicle called Mutual Funds : Chapter 6

A vehicle called Mutual Funds talks about what you should consider while selecting a good equity mutual fund for a long term. They suggest tagging your investments to Goals. The most important step is to have an investment goal. You should know the reason for your investment, how long you can stay invested, at what stage you will re-allocate etc before you invest.

- Liquid Funds ==> Short term goals

- Equity Funds ==> Long Term Goals

- Income Funds ==> Medium Term Goals.

Life and Health Insurance : Chapter 8

Insurance- Life or general – is largely about answering the question “What if something goes wrong?” You are paying an insurance premium ( a small cost) to avoid paying the total cost for a catastrophic loss, such as your house burning down. So it is fairly obvious that you will not insure your mobile phone (you can afford to carry the risk on your own self) but you will insure your house (the burden of this risk is too heavy to carry). So you transfer the risk associated with the loss of a house by paying a premium, the risk of the loss of a mobile, you keep with you.

It then gets down to questions like

- How much insurance do you really need? – Does my family really need Rs 6 crore on my death?” It reminds that Insurance is not because you will die;it is because they will live.

- What is you stop paying premiums and let your policy lapse? Ask your self the following questions:

- Why did you purchase this policy? Was it to help protect my family’s future by replacing my income if I died prematurely? Make sure that education funds are available for my children? Retire the mortgage or pay off other debts?

Records to be maintained : Chapter 9

It answers the question: Why we should be particular about the record keeping of your income, expenses, investments , taxation etc? and suggests to Pick a system, any system. Paper work piles up fast.

Record keeping is necessary (nay compulsory) for 3 main purposes

- Tax returns filing

- Investment performance tracking

- Goals monitoring

Mistakes to be avoided : Chapter 10

The longest chapter of the book which runs into 20 pages. Warren Buffet is reckoned to have said “It’s good to learn from your mistakes. It’s better to learn from other people’s mistakes” Mistakes that are covered are:

- The kind of investment mistakes that I have made myself

- The kind of investment mistakes that I have seen people make

- The kind of mistakes you could make with regard to insurance

- My own attitude towards mistakes

- Knowing how to avoid making those mistakes.

It also talks about Listening to parents about investing : This is one of the worst crimes that some of you can commit. Especially true if your parents are PPF-LIC-Bank FD-type of savers.

A gem in this chapter is how to Stay away from new products. One of the most important lessons in the Goal Based Investing is when a financial product is offered to you, learn to ask few questions

- Am I able to understand the product?

- Do I know what the product serves?

- Do I already have a product for that purpose?

- With who can I discuss the merits or demerits of the product?

- Who regulates such products, RBI/SEBI/IRDA/PFRDA?

- Can I achieve the same result by investing more in one of the products that I already have

- Which goal will it help

- Is this any investment or protection

- I already have enough protection so do I still need it

- My investments are already channelled into SIPs so do I have any more money to invest?

Normally once you the following

- Savings Bank account(normally one is enough)

- Credit card (not more than two)

- Term insurance and Health Insurance (keep reviewing the adequcy)

- Mutual funds (a maximum of 5)

You should start saying NO to every product that is offered to you. Just say No. In fact this is one word which will make you RICH.

More about Mutual Funds: Appendix 1

Talks about Salient features of mutual funds, Equity Mutual Funds, Fund Selection, Dangers of using Star Ratings to select or review mutual funds, The role of a mutual fund manager, Measuring mutual fund performance.

Appendix 2 : Description of Calculators

The following calculators can be accessed by registering at special site mentioned in the book,a kind of bonus on buying the book. Additional resources mentioned in the book are at https://freefincal.com/tools/

- Net worth calculator

- Life insurance calculators

- Financial goal planner with variable asset allocation

- Monthly investment tracker

- Time value of money calculator

- True power of compounding

- Impact of 1% (difference in return calculator)

- Cost of delay (in investing calculator)

- Visual goal planning and asset allocation

You Can Be Rich With Goal-based Investing

Should you buy the book, You Can Be Rich With Goal-based Investing. We believe You will be the same person in five years as you are today except for the people you meet and the books you read. This book is a simple full of common sense, practical questions and solutions. No mathematics equations, good and appropriate pictures. We have given highlights of the book (see we have read the book :-)) and you can try out the calculators too. There are many books in the market regarding Indian Finance and the money in buying book is well spent.

Related Articles:

- Personal Finance Books For Adults And Young Adults in India

- Book Review-JagoInvestor:16 personal finance principles every investor should know

- Books on Money for Children

- Robert Kiyosaki’s Rich Dad Poor Dad : Is it good personal finance book?

- Secrets of Millionaire Mind : How Rich and Poor People think differently

Do you read books on personal finance? Which books in personal finance do you like? What are the good ways to learn about personal finance? What is the most difficult aspect of personal finance?

One response to “Review of the Book : You Can Be Rich With Goal based Investing”

[…] Review of the Book : You Can Be Rich With Goal based Investing […]