Before or On retirement the question that one has is how to use the retirement kitty? You are or will be retired and are looking forward to living a relaxed life. Collecting your pension and provident fund money is work half-done. You have to plan meticulously to not only make your money yield returns that are higher than inflation but also minimise the amount you have to pay as tax. To ensure a regular stream of income, you need to deploy your retirement corpus in the the right products. We look at the various investment options suited for retirement savings.

A relaxed life after retirement can be achieved by smart financial planning to give you the financial security needed in old age On retirement, an employee normally receives certain retirement benefits. In the year one receives the retirement benefits. Such benefits are taxable under the head ‘Salaries’ as ‘profits in lieu of Salaries’ as provided in section 17(3). However, in respect of some of them, exemption from taxation is granted u/s 10 of the Income Tax Act, either wholly or partly. Please use those.

Table of Contents

Planning For Post Retirement

Plan for your retirement by using following steps. Try to be in control of your finances, include your children if you trust them or their spouse. Do not give away your property and assets to your children while you or your spouse is alive. Make a will on how to distribute your financial assets.

Step one of retirement planning is to quantify how much savings one has accumulated before retirement.

To mention few savings: provident fund, gratuity, fixed deposits, shares, term insurance, cash in savings account etc. Suppose provident fund is Rs 30 Lakhs, Gratuity is Rs 15 lakhs, Fixed Deposit is Rs 5 Lakhs, Share is Rs 3 Lakhs & Term Insurance is Rs 3 Lakhs, cash is Rs 2 Lakhs. Adding up all these savings it amounts to Rs 58 Lakhs. Idea is to quantify how much retirement money does one have? Proper investment of this money has to be done to generate for future.

Step two is to account expenses(monthly and annual)

No matter how judiciously we save there will be some expenses. We can never cut our expenses down to zero. But if we start to dig into our savings ultimately it will get finished. Idea of doing this exercise is to exactly know how much we will need to dig into our retirement money each month. This is where careful investment of retirement money is important.Target is to generate fixed income without digging into principal amount (retirement money). In our example, adding all expenses, it amounts to Rs 31,500/month.

Step three to see is pension or annuity enough to take care of your expenses for at least the first few years in retirement?

If not, how much extra income is required? For example, if average monthly expenses is 30,000 and 23,000 is the monthly pension, about 7,000 is the income to be generated from retirement savings. If there is no pension then in our above example retirement savings is Rs 58 Lakhs and monthly expense is Rs 31,500. In order to generate Rs 31,500 per month from savings of Rs 58 lakhs, return @ 6.5% per annum is required.

Step 4: What is your tax slab?

Retirement does not mean the end of income. So, it is important to identify the sources of income on which you have to pay tax. Other than pension, tax is payable on income from property, that is, rent; capital gains (long and short term); and dividend and interest from equity and fixed-income investments. if you are working post retirement then Income from salary is also taxed. In order to minimise tax, invest in products wherein either the yearly outflow or the maturity amount is taxfree. Our article Senior Citizen : Income and Tax discusses it in detail.

Pension is also taxed as per the tax slabs for senior (60 years and above) and very senior citizens (80 years and above), depending on whether it is received as a lump sum (commuted) or in a staggered manner. Commutation means payment of a lump sum in lieu of surrender of a part of the pension.

- Commuted pension for government employees is exempt from tax. However, for non-government employees, one-third pension is exempt if they have received gratuity and half is exempt if they have not received gratuity.

- Non-commuted pension is taxed at the prevalent rate.

Please note Resident senior citizens who do not have any income from business or profession are exempted from payment of advance tax, irrespective of tax liability quantum

Form 15H and 15G One can submit forms 15H and 15G to avoid tax deduction at source. A person who is 60 years or more can submit Form 15H, but only if he/she has not paid tax in the previous assessment year. The form must be submitted at the start of the financial year. Form 15G is for individuals below 60 years of age and Hindu undivided families. Our article How to Fill Form 15G? How to Fill Form 15H? discusses it in detail.

Things to keep in mind while investing Retirement money

As majority of individuals in this age bracket stop earning, it becomes a priority to ensure a source of regular income and have investments that are more liquid to meet any untoward emergency. Cash flow needs can be covered through a combination of rent, dividend, interest income and systematic withdrawal plans (SWP). Some pointers to keep in mind while investing post retirement.

- As a senior citizen, while safety of capital is paramount, don’t forget to take into account the tax factor. Taxes can actually erode the value of your returns.

- Also another black hole to watch out for is inflation. Many seniors opt for the security of assured returns and end up finding that the value of their investment has eroded due to inflation.

- Investments with long lock in period should be avoided.

- Have contingency funds for medical emergencies and health checkups

Investments should be made be across assets which enhances wealth and also makes returns more predictable. Besides having allocation towards safe debt products which caters to cash flow requirements, do not avoid equity-oriented investments.Retirees think they are taking risk by investing in equity. However, one should limit their exposure to 20-30% in equity, ideally through mutual funds to own an inflation beating portfolio. One needs to strike a balance between traditional and market-related investments.

Investment Options on Retirement

Retirement planning has become synonymous with investing in avenues with guaranteed and secure returns. However, one must realise that in the bargain most end up opting for instruments that not only generate low returns but are also least tax-efficient. What needs to be done is to strike a balance between traditional and market-related investments. Given below are the options where one can invest one’s retirement corpus.

Senior Citizens’ Savings Scheme (SCSS)

This is a savings scheme launched by the Indian government particularly for senior citizens. Our article Senior Citizen Savings Scheme, SCSS discusses it in detail.

- All seniors above the age of 60 years can invest in this scheme. Those who are above 55 years of age are also eligible to invest in this scheme but are subject to certain conditions.

- The scheme has a lower limit of Rs 1,000 and an upper limit of Rs 15,00,000.

- One can invest up to Rs 15 lakh through post offices or designated public sector banks.

- The scheme has a period of 5 years and carries an interest rate of around 9 per cent. The five-year lock-in period can be extended for another three years.

- The interest is credited to the account on March 31, June 30, September 30 and December 31.

- The investment in Senior Citizen Scheme (only the first investment) qualifies for deduction under Section 80C of the Income Tax Act.

- TDS If the income earned is over Rs 10,000, tax is deducted at source.

- A penalty of 1.5 per cent is applicable on the amount deposited in case the deposit is withdrawn before 2 years and 1 per cent if the amount is withdrawn after 2 years but before the expiry of the term.

Post Office Monthly Income Scheme (POMIS)

- Are you looking for a guaranteed monthly income? Then monthly income scheme (MIS) offered by various post offices in the country is best suitable for you.

- You can invest a minimum of Rs 1,000 and a maximum Rs 4.5 lakh for a single account and Rs 9 lakh for a joint account.

- You earn around 8 per cent interest when you are invested. The interest rate is a tad lower than the SCSS.

- The maturity period is six years.

- The return is credited to a designated account on a monthly basis. One can collect the payment from the post office or transfer the amount to the bank account electronically

- If you withdraw after a year, a penalty of 5 per cent of the amount deposited is applicable. However, there is no penalty after 3 years.

- The account can be easily transferred to another post office.

- The returns are added to the income and taxed as per one’s income tax slab.

Post Office Time Deposit (POTD)

This is similar to the term deposit offered by banks. Since the investment is backed by the government of India, it is risk-free and offers guaranteed returns.

- The minimum amount to be deposited in this scheme is Rs 200 and, thereafter, in multiples of Rs 200. and there is no limit on the maximum amount than can be deposited.

- The period for the deposit ranges from 1 year to 5 years and the interest rate ranges from 6.25 to 7 per cent, compounded quarterly.

- .The interest payout is annual.

- Here, too, the interest income is subject to tax, though tax is not deducted at source.T

- he five-year deposit is eligible for tax deduction under Section 80C of the Income Tax Act.

Fixed Deposits (FD)

Offered by various banks and companies they have been the most sought after by those looking for safe returns.. Though the interest rates on the bank deposits are lower than the interest rates on company deposits, bank deposits are safer. Always choose deposits with AAA rating, as they are the safest from amongst all the deposits. Our article Senior Citizen,Fixed Deposits and Tax discusses it in detail.

- There is no minimum investment requirement.

- Senior citizens get 0.25-0.5 per cent over and above the regular rate.

- The tenure can be a mere week to 10 years.

- The applicant can opt for crediting of interest to a savings bank account on quarterly, semiannual or annual basis.

- There is also an option for re-investment of interest.

- Barring for tenures of five years and above, bank FDs do not enjoy any tax exemption. The long term FD (five year-plus), which is eligible for deduction under Section 80C, cannot be liquidated in the middle of the term and, hence, is illiquid.

- Tax:The interest attracts TDS and cess if it is more than Rs 10,000 in a financial year. One must note that the risk is low only as long as the bank is in a good financial shape. In case the bank goes bust, only Rs 1,00,000 is guaranteed (by the Deposit Insurance and Credit Guarantee Corporation).

Pradhan Mantri Vaya Vandana Yojana

On 4 May 2017 Pradhan Mantri Vaya Vandana Yojana (PMVVY) was open for those above 60 years with the assured return of 8%. Our article Varishtha Pension Bima Yojana 2017,Pension Plan for Senior Citizens dicsusses it in detail.

- You pay premium only once in lump sum called as Purchase Price.

- You will get pension monthly, quarterly, half-yearly or annually for 10 years.

- Min pension is Rs 1000 monthly and maximum pension you can get is Rs 5000 monthly.

- On Maturity, you will get the full amount. On death, your nominee will get the purchase price back

- The scheme will be implemented through Life Insurance Corporation of India (LIC) from 4 May 2017 to 03-May-2018.

- No tax benefits on the Purchase price or premium contribution of PMVVY under Section 80C.

- The pension amount is a taxable income in the hands of pensioners.

Monthly Income Plans (MIP)

Debt mutual funds, especially monthly income plans and liquid funds are ideal assets for senior citizens to invest in. They offer capital protection for moderate returns, are liquid, and also have the benefit of providing regular income streams. Since senior citizens enjoy a higher tax cover, there may not be any tax implications on these investments (depending on one’s investment levels, etc.)

Monthly Income Plans are market linked investment options offered by mutual funds. These are best for those who are conservative but still want some exposure to equity markets.

- These are open-ended schemes that invest most of their money in debt instruments. Only a small portion is put in equities.

- The regular income comes from dividend payouts. However, unlike post office plans, where returns are guaranteed, there is no such surety about dividends from mutual funds. These are paid either on monthly, quarterly or on annual basis. Also, the amount is not fixed. The dividend is not taxed but redemptions are taxable as per capital gains rules.

- Redemption before three years attracts short-term capital gains tax. Profits from MIPs sold after three years are considered long-term capital gains and taxed accordingly, that is, subjected to a flat tax rate of 20 per cent with indexation.

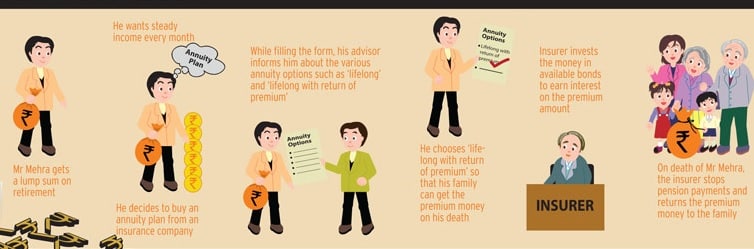

Annuities

An individual should essentially have one pension plan in addition the other investment options to have a regular source of income after retirement. Pension plans are available for people up to the age of 80 years. Investment in a pension plan can be performed in two ways. One, by depositing a lump sum amount and later receiving the money as monthly payouts inclusive of interest earned; secondly, by depositing money quarterly that will be provided either as lump sum or monthly, depending on your choice.

Public Provident Fund

Though PPF is mainly the preferred route for building a corpus for retirement because of its tax benefits, it can also be used to park a part of the final corpus, preferably by extending the existing account in blocks of five years instead of opening a fresh account and locking the money for 15 years.

- One can invest up to Rs 1,50,000 every year in PPF. It has a lock-in of 15 years. However, one can extend the account three times after the end of the 15th year in a lot of five years.

- You can withdraw a part of the corpus from seventh year. This amount cannot exceed 50 per cent of the corpus at the end of the preceding year. You can also take a loan against the corpus from third-year onwards. The rate for this is two percentage points more than what is offered to investors.

- Public Provident Fund (PPF) is among the few options exempt from tax at both investment and maturity stages under Section 80 C and Section 10 (10D) of the Income Tax Act, respectively. PPF investments also qualify for deduction under Section 80 C of the Income Tax Act. This reduces the overall tax burden.

Reverse Mortgage

Reverse mortgage provides regular income or interest in exchange of the property. This is a product for those who have real estate but not much free cash.

- In this, the retired person keeps a house as collateral with the bank.

- In return, the bank makes monthly payments according to the value of the house.

- During the receipt of regular income, the borrower can continue to live in the property.

- The borrower can opt for monthly, quarterly, annual or lump sum payments.As reverse mortgage is a loan, the interest rate is either fixed or floating.

- The payments are not taxable. This is because the amount received from the bank is considered a loan and not income.

- As per the RBI guidelines, the maximum period for which the property can be mortgaged is 20 years, after which either the borrower or the heir (in case of the death of the borrower) can either repay the loan or sell the house and settle the transaction. The excess amount generated in the process is passed on to the borrower or the heir.

- The borrower can also claim back the property by paying higher rate of interest.

A home is generally one of a retiree’s biggest assets, and a reverse mortgage is a means by which you, as a retiree, can utilize that asset when you want to. What is a reverse mortgage going to do to help you? If you find yourself short on funds during retirement but own your own home then you are sitting on unusable funds in the form of your home’s value. A reverse loan is simply a way to turn those unusable funds into money you can actually spend. You can do that by requesting monthly installment payments to help you pay ongoing bills or a lump sum payment to cover some sort of emergency expense. The choice is yours. Regardless of how you use the reverse loan funds, repayment of the loan will not be expected until your death, unless you choose to move out of your home.

NSC (National Savings Certificates)

In NSC scheme one can invest for duration of 5 years. NSC (IX issue) with maturity period of 10 years discontinued with effect from 20th December 2015. Our article What are National Savings Certificate (NSC) discusses NSC in detail

- Once invested into NSC, withdrawal is only possible after 3 years.

- Amount invested is eligible for deduction under Section 80C. Interest accrued during the year except for the last year is deemed to be reinvested and shall also qualify for deduction under Section 80C.

- No TDS is deducted on repayment.

Fixed Maturity Plans (FMP)

FMPs are close-ended debt mutual funds with tenures ranging from three months to three years.

- These are close-ended and cannot be redeemed like other mutual funds before maturity. They are listed on exchanges where they can be bought or sold, though they are a highly illiquid investment.

- Even though liquidity is an issue, the one factor on which FMPs triumph over FDs is returns. It has been observed that debt mutual funds give returns that are 50-100 basis points more than what is paid by FDs.

- Also, FMPs are more tax efficient for tenures over three years as they enjoy indexation benefits with a fl at 20 per cent tax rate.

- Given their structure, FMPs are more suitable for individuals in the 30 per cent tax bracket. If the investment is for one to three years, the investor has to add the gains to his/her income and pay tax according to her/his income tax bracket.

Equity Mutual Funds and SWP

You need to generate inflation adjusted returns and debt assets cannot do that consistently. Long term capital gains (on redemption after a year) from stocks and equity mutual funds are not taxed. Hence, these two products are ideal for investing a part of the corpus. You need to have some equity exposure. However, experts say one must avoid over-exposure to stocks after retirement because they are risky.

- Dividends from stocks and equity mutual funds are tax-free.

- Short-term capital gains, that is, profits made by selling within a year of purchase, attract 15 per cent tax. To avoid this, invest in stocks for the long term.

- Through STP, one can invest a lump sum in a particular fund (say debt) and, thereafter, transfer a fixed sum regularly to another mutual fund (say equity). This ensures that your corpus starts with the safety of a debt fund even as you slowly keep increasing exposure to equity funds.

SWP IN MIPS To tide over the uncertainty over dividend payments in MIPs, investors can opt for systematic withdrawal plans (SWPs). In SWP, you can choose the frequency and quantum of payments. If the scheme fails to generate returns that match the agreed payout, you will be paid from the principal amount. In SWP, the investor is liable to pay short- and long-term capital gains tax.

Comparison of Post Retirement Investment Options

Comparison of few retirement options are as follows:

| PMVV | Fixed Deposit | Senior Citizen Saving Scheme | POTD | NSC | Mutual Funds | Pensions Plans | |

| Minimum Investment | 1,44,578 | Rs 1000 | Rs 1,000 | Rs 200 | Rs 100 | Rs 500 | Rs 200 |

| Maximum Investment | 7,50,000 | No upper limit | Rs 15 lakh | No upper limit | No upper limit | No upper limit | No upper limit |

| Investment tenure | 10 years | 7 days-10 years | Up to 8 years | 1-5 years | 5-10 years | Can be both short and long-term | Can be both short and long term |

| Lock-in period | 10 years | Same as tenure | 5 years | Same as tenure | Same as tenure | 3 years | 3 years |

| Rate of interest | 8% | 6%-8% | around 8.5% | 7-8% | around 8% | Market-linked | 3%-7%(depends on the issuer) |

| Penalty on premature withdrawal | 2% | Interest rate applicable will be 1% less than the original rate. | 1%-1.5% | Interest paid will be according to the postal saving scheme and not as per the plan. | No premature withdrawal allowed | No premature withdrawal allowed | No premature withdrawal allowed |

| Tax status | No tax benefit | EET | EET | EET | EET | EET | EET |

Related Articles

- Senior Citizen,Fixed Deposits and Tax

- SCSS or Senior Citizen Savings Scheme

- Income and Tax for Senior Citizen

- Senior Citizen Term Deposits – Features, Benefits & Rates

- How to Fill Form 15G? How to Fill Form 15H?

[poll id=”94″]

Retired life is supposed to be the golden period of our lives, and if we manage our money with some rules, we will be able to enjoy it as well. You must evaluate your tax liabilities before selecting the investment options. Try and strike a balance between tax-saving, income generation and safety.

3 responses to “Senior Citizen and How to invest Retirement money?”

Undeniably imagine that which you said. Your favorite reason seemed to be at the internet the simplest thing to be mindful of. I say to you, I certainly get annoyed even as other folks think about concerns that they just do not know about. You managed to hit the nail upon the highest and defined out the entire thing with no need side-effects , people could take a signal. Will probably be back to get more. Thank you

Interest rates mentioned at comparison need to be updated FD rates are 6 to 7.8 %, Senior Citizen Saving Scheme is now 8.5 % , Post TD are 7 to 7.8 %, NSC is 8 %

Thanks for comment. Updated.