If you have sold house, property, land or building, also called as immovable property after 3 years then you have Long term Capital Gains and have to fill Schedule CG in ITR2, ITR3 etc. This article talks about how to show Long Term Capital Gain on sale of house in ITR or Income Tax Return.

Table of Contents

Short and Long Term Capital Gains on Sale of Property

Capital gains arising from sale/transfer of different types of capital assets have been segregated. If more than one capital asset within the same type has been transferred, make the combined computation for all such assets within the same type.

- If a property is sold within three years of buying it, it is treated as a short-term capital gain. This is added to the total income and taxed according to the slab rate.

- If a property is sold after three years from the date of purchase, the profit is treated as a long-term capital gain and is taxed at 20% after indexation .

- If you took property on home loan, claimed the tax deduction for the principal under Section 80C and property is sold within five years, the tax benefits will be reversed. The entire tax deduction ,for repayment of principal component of the home loan ,claimed in earlier years under section 80c , will be considered as your income (in addition to capital gains) in the year in which you sell the property. However, the housing loan interest deduction claimed under section 24(b) won’t be reversed.

Long Term Capital Gains on Sale of House in ITR

Which ITRs have Schedule for Capital Gains?

One has to fill schedule CG or Capital Gains in ITRs. ITR2, ITR3,ITR4S, ITR4 have capital Gains section. So if are individual or HUF and you have sold land,property, gold,debt mutual funds you have capital gain ,long or short, you cannot use ITR1 and ITR2A.

Remember when you own a house/houses you have Income from House Property.Income from House Property and Income Tax Return explains how to show house property in ITR. Only when you sell the house you will have capital gain.

Schedule CG in ITR

The schedule CG is divided in two parts. The short term capital gains and long term capital gains. The section 1 in Long Term Capital Gain,is for the reporting of capital gains on property. If you have sold a property after three years of purchase, you must fill this section. The income tax department also considers the inflation effect in your investment. It does not want to tax on the price increase just because of the inflation. Therefore, indexing is used to get the purchase cost at today’s price.

Raj purchased a piece of land in May, 2004 for Rs. 84,000 and sold the same in Dec, 2015 for Rs. 10,10,000 (brokerage Rs. 10,000). He invested 8,00,000 in buying a new house in May 2016. What will be the taxable capital gain in the hands of Raj?

Computation of capital gain will be as follows , CII of the Purchase Year: 2004 month: May : 480 CII of the Sale Year: 2015 month: Sep : 1081

- Full value of consideration (i.e., Sales consideration of asset) 10,10,000

- Less: Expenditure incurred wholly and exclusively in connection with transfer of capital asset (brokerage) 10,000

- Net sale consideration 10,00,000

- Less: Indexed cost of acquisition (*) 189175 (84,000 * 1081/480)

- Less: Indexed cost of improvement, if any Nil

- As he bought a new house within 2 years from selling his old house he can claim Exemption under section 54 of Rs 8,00,000

- Long-Term Capital Gains 8,025

- So tax on his long term capital gain is 20% of long term capital gains which is 1605.

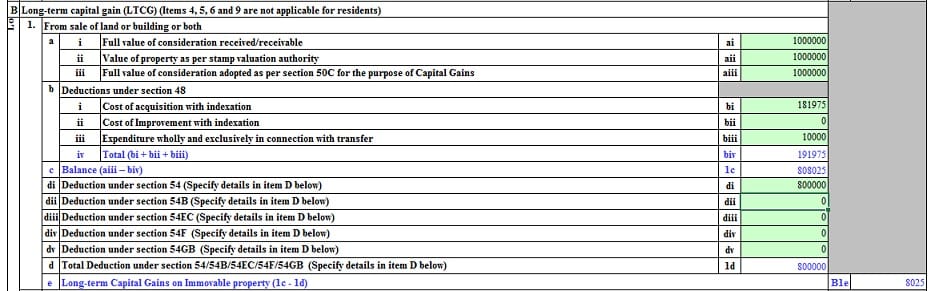

This will be shown in ITR as shown in image below.

Long-Term Capital Gains on sale of house in ITR

The explanation to fill various fields are as follows:

- You are required to give the sale value of the property in sub section ‘a(i)’.

- You must fill the value of the property ascertained by the stamp valuation authority. You will get this value at the time of property registration.

- In the column a(iii) you are required to fill the value which is greater of the sale value and the ascertained value.

- In the sub section you should give the cost incurred by you corresponding to the inflation. For computing long-term capital gain, cost of acquisition and cost of improvement may be indexed, if required, on the basis of following cost inflation index notified by the Central Government . The cost inflation index notified for the year 2004-05 is 480 and for the year 2016-17 is 1081.Hence, the indexed cost of acquisition, i.e., the inflated cost of acquisition will be computed as follows: Cost of acquisition × Cost inflation index of the year of transfer of capital asset /Cost inflation index of the year of acquisition = 84,000 * 1081/480. Cost Inflation Index Up to FY 2016-17 can be used to find the indexation of a Financial Year. You can use our Capital Gain Calculator .

- The improvement cost of property is also given with the indexation.

- you must give the Expenditure transaction cost (stamp duty, brokerage etc) as well

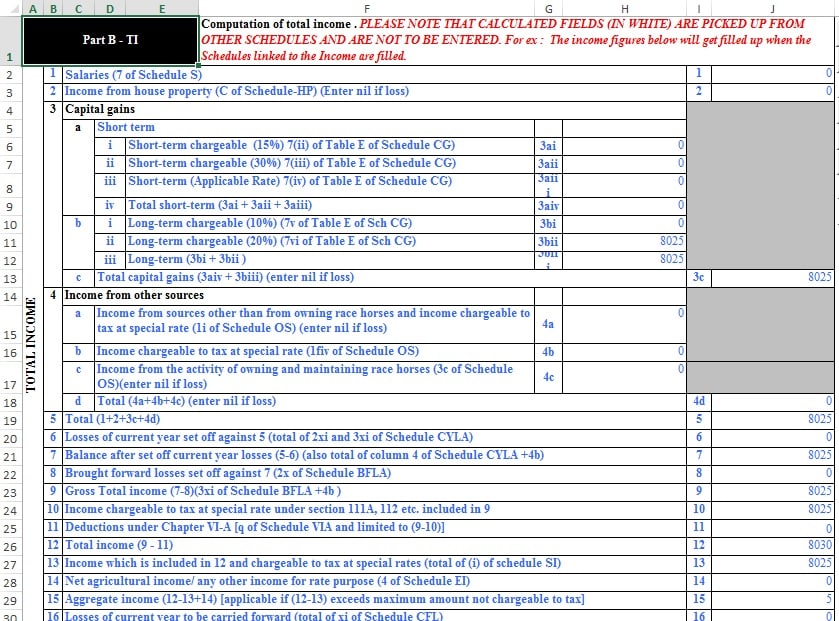

Long Term capital gain in Total Income of ITR will show up in Capital Gains as 3bii. This is a simple case in which we are just considering Long Term Capital Gain. Actually you will have other type of income too.

Long term Capital gain from sale of house in ITR in Total income section

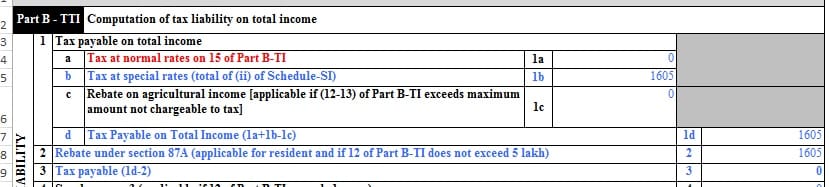

Computation of Tax on Loan Term Capital Gain on Sale of House is 20% of the long term capital gain. Following image shows the tax liability on long term capital gains in ITR

Long-Term Capital Gains from sale of house in ITR

Section 54: Exemption for Capital Gains

A person wanted to shift his residence due to certain reason, hence, he sold his old house and from the sale proceeds he purchased another house. In this case the objective of the seller was not to earn income by sale of old house but to acquire another suitable house. Section 54 gives relief to a taxpayer who sells his residential house and from the sale proceeds he acquires another residential house. Following conditions should be satisfied to claim the benefit of section 54. There are other sections like 54/ 54B/ 54D/ 54EC/ 54F/54GB/115F which are explained later.

- The benefit of section 54 is available only to an individual or HUF.

- The asset transferred should be a long-term capital asset, being a residential house property.

- Exemption under section 54 will be lower of following : Amount of capital gains arising on transfer of residential house; or Amount invested in purchase/construction of new residential house property.

- The benefit of section 54 is not available if the capital gain arising on transfer of house is invested another house and not in capital asset other than a residential house. if one wants to purchase a shop (i.e., capital asset other than a residential house)

- Within a period of one year before or two years after the date of transfer of old house, the taxpayer should acquire another residential house or should construct a residential house within a period of three years from the date of transfer of the old house. In case of compulsory acquisition the period of acquisition or construction will be determined from the date of receipt of compensation (whether original or additional).

- If till the date of filing the return of income, the capital gain arising on transfer of the house is not utilised (in whole or in part) to purchase or construct another house, then the benefit of exemption can be availed by depositing the unutilised amount in Capital Gains Deposit Account Scheme in any branch of public sector bank, in accordance with Capital Gains Deposit Accounts Scheme, 1988 (hereafter referred as Capital Gains Account Scheme). The new house can be purchased or constructed by withdrawing the amount from the said account within the specified time-limit of 2 years or 3 years, as the case may be.

- With effect from assessment year 2015-16 exemption can be claimed only in respect of one residential house property purchased/constructed in India. If more than one house is purchased or constructed, then exemption under section 54 will be available in respect of one house only. No exemption can be claimed.

Shyamli purchased a residential house in April, 2011 and sold the same on 25th April, 2016 for Rs. 8,40,000. Capital gain arising on sale of house amounted to Rs. 1,00,000. Out of the sale proceeds of old house, she purchased another residential house for Rs. 80,000. This house was purchased in Dec, 2015. What will the long term capital Gain?

- Exemption under section 54 can be claimed in respect of capital gains arising on transfer of capital asset, being long-term residential house property, which is applicable to Shyamali.

- Exemption will be lower of the following amount : Amount of capital gain, i.e., Rs. 1,00,000. Amount of investment in new house, i.e., Rs. 80,000 Thus, exemption will be Rs. 80,000.

- Taxable capital gain will come to Rs. 20,000 (Rs. 1,00,000 less exemption under section 54 of Rs. 80,000).

Aryan purchased a residential house in April, 2011 and sold the same on 25th April, 2016 for Rs 8,40,000. Capital gain arising on sale of house amounted to Rs. 1,00,000. Out of the sale proceeds of old house, he purchased another residential house for Rs 1,20,000. This house was purchased in Oct, 2015. What will be the amount of exemption under section 54 which can be claimed by Aryan?

- Exemption under section 54 can be claimed in respect of capital gains arising on transfer of capital asset, being long-term residential house property.

- The exemption will be lower of the following amount : Amount of capital gain, i.e., Rs. 1,00,000. Amount of investment in new house, i.e., Rs. 1,20,000 .Thus, exemption will be Rs. 1,00,000.

- Taxable capital gain will come to Nil (entire gain will be exempt).

Long Term Capital Gain – Exemption under section 54/ 54B/ 54D/ 54EC/ 54F/54GB/115F

The following table gives overview of sections of capital gain exemption. When one sells a residential house one can claim exemption under section 54.

| Section | Who can claim exemption | Eligible assets sold |

| 54 | Ind/HUF | A residential House property (minimum holding period 3 year) |

| 54B | Individual /HUF wef AY 13-14 | Agriculture land which has been used by assessee himself or by his parents for agriculture purposes during last 2 yrs of transfer |

| 54EC | Any person | Any long-term capital assets (minimum holding period 3 years) |

| 54F | Ind/HUF | Any long term asset (other than a residential house property ) |

TDS on Property

The buyer of an immovable property, valued at Rs 50 lakh or more, is required to pay TDS to the government. It comes under the Sec 194 IA, the Income Tax Act 1961. The rate at which the buyer needs to deduct tax is 1% and it may go up to as high as 20% if the seller does not disclose his PAN. If the property purchased is for Rs. 70 Lakhs then one needs to pay tax on full amount i.e 70 lakh not only on amount more than 50 lakh i.e. Rs. 20 Lakhs. In this example if buyer knows PAN of seller then buyer would need to submit TDS @1% of 70 lakh i.e 7 lakh. Note unlike the Self assessment Tax ,No surcharge and education cess is applicable while deducting tax on sale of property.

If property is bought from Non-Resident Indian (NRI) then section 194-IA will not be applicable but section 195 will come into action. For NRI the limit of Rs 50 lakh is not applicable. If property is bought from NRI, TDS is required to be deducted at the rate of 20% plus Education Cess on the sale amount. Surcharge at the rate of 10% will be applicable if amount paid exceeds Rs 1 crore.

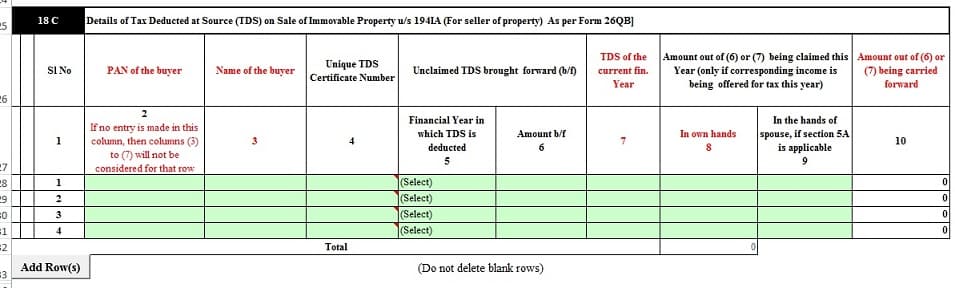

As you know Form 26AS tracks the tax paid to government, TDS on salary, advance, self assessment tax. So even TDS on Sale of property shows up in Form 26AS seven days after payment as shown im image below

- For Seller of property TDS is reflect in Part A2 under Details of Tax Deducted at Source on Sale of Immoveable Property u/s 194(IA) [For Seller of Property]

- For Buyer TDS is reflected in Part F under Details of Tax Deducted at Source on Sale of Immoveable Property u/s 194(IA) [For Buyer of Property].

TDS for sale of Property in ITR

Adjustment of LTCG against the basic exemption limit

Can an individual adjust the basic exemption limit against long-term capital gain? The answer will depend on the residential status of the individual (i.e., resident or non-resident).

Only a resident individual/HUF can adjust the exemption limit against LTCG. Thus, a non-resident individual and non-resident HUF cannot adjust the exemption limit against LTCG. A resident individual can adjust the LTCG but such adjustment is possible only after making adjustment of other income. In other words, first income other than LTCG is to be adjusted against the exemption limit and then the remaining limit (if any) can be adjusted against LTCG.

Ranbir (age 67 years and resident) is a retired person. He purchased a piece of land in December, 2010 and sold the same in April, 2015. Taxable long-term capital gain on such sale amounted to Rs. 1,84,000. Apart from gain on sale of land, he is not having any other income. What will be his tax liability for the AY 2016-17?

For resident individual of the age of 60 years and above but below 80 years, the basic exemption limit is Rs. 3,00,000. Further, a resident individual can adjust the basic exemption limit against LTCG. In this case, LTCG of Rs. 1,84,000 can be adjusted against the basic exemption limit. So Ranbir can adjust the LTCG on sale of land against the basic exemption limit. Considering the above discussion, the tax liability of Ranbir for the AY 2016-17 will be nil.

Long Term Capital Gains and Deductions under sections 80C to 80U

No deduction under sections 80C to 80U is allowed from long-term capital gains.

Aarti (age 57 years and resident) is a retired person. She purchased a piece of land in December, 2010 and sold the same in April, 2015. Taxable LTCG on such sale amounted to Rs. 4,00,000. Apart from gain on sale of land she is not having any income. She deposited Rs. 1,00,000 in Public Provident Fund (PPF) and Rs. 50,000 in NSC. She wants to claim deduction under section 80C on account of Rs. 1,50,000 deposited in PPF and NSC. Can she do so?

She can claim basic exemption of Rs. 2,50,000 (being resident individual) and has to pay LTCG on remaining Rs. 1,50,000 @ 20% (+ Ed. Cess+ SHEC). Thus, her tax liability before cess will come to Rs. 30,000 and after deducting rebate of Rs. 5,000 as per section 87A, he would be liable to pay tax of Rs. 25,750 (including cess @ 2% and 1%).

Related Articles:

- List of articles to Understand Income Tax, Fill ITR,Income Tax Notice

- How To Fill Salary Details in ITR2, ITR1

- How to Fill ITR when you have multiple Form 16

- Filing ITR : Video on Steps to File ITR, Ways to File,Documents required

How to calculate CG on house purchased in 1993 and sold 2019

Hey! It comes under the Sec 194 IA, the Income Tax Act 1961.